Are Vet Wellness Plans Worth It? An Honest Breakdown

Claire Greenway

BVM&S MRCVS

At some point, usually at the desk after an appointment, someone at your vet practice will offer you a monthly plan. A Healthy Pet Club, a Pet Health Club, a wellness plan, the names vary but the pitch is the same: pay a set amount each month and get your pet's routine preventive care bundled in, often with discounts on top. It sounds tidy, and the monthly figure usually sounds small. So is it actually worth it?

Here's how we're going to handle this, because it's a question that attracts a lot of strong opinions and not much straight arithmetic. We're not going to tell you these plans are a con, because for a lot of owners they genuinely aren't. And we're not going to tell you to sign up, because for some pets they're poor value. What we'll do instead is show you exactly what's usually inside a plan, how to work out whether the maths adds up for your pet, and the one bias built into almost every plan that you should factor in. Then you can decide.

One thing to get clear straight away, because owners muddle these constantly: a wellness plan is not insurance. Insurance pays towards unexpected illness and injury. A wellness plan spreads the cost of routine, expected preventive care. They do different jobs, and a plan is no substitute for cover when something serious and costly goes wrong. If you're weighing up insurance, that's a separate decision covered in our how-to-choose insurance framework.

What's actually inside a wellness plan

Plans vary between practices, but the typical bundle is some combination of the following, spread across the year for one monthly fee:

- Annual vaccinations (the booster appointment)

- Year-round flea and tick treatment

- Year-round worming treatment

- One or two health checks a year with a vet or nurse

- Sometimes nail clips, anal gland checks, or a nurse clinic

- A discount on other practice services, food, or dentals

The appeal is real. You spread predictable costs into manageable monthly amounts, you never forget the flea and worm treatment because it's handed to you, and you feel organised. For a lot of busy households, that convenience alone has value.

But notice something about that list. Almost every item on it is a product or a routine service the practice provides anyway. The plan isn't creating value out of nothing, it's bundling things you might buy piecemeal into a subscription. Whether that's a saving or a premium depends entirely on how the bundle is priced against what you'd otherwise spend, and on whether your pet actually needs everything in the bundle.

How to work out if it's worth it, for your pet

This is the part that turns a gut feeling into an answer. Do a quick sum, once, on the back of an envelope.

Step one: total the monthly fee for the year. Multiply the monthly cost by twelve. That's what the plan costs you.

Step two: price the same items bought separately. Ask the practice, or check, what the booster, the flea treatment, the worming, and the health checks would cost if you paid for each as you went. Add them up honestly, including the things you'd genuinely buy anyway.

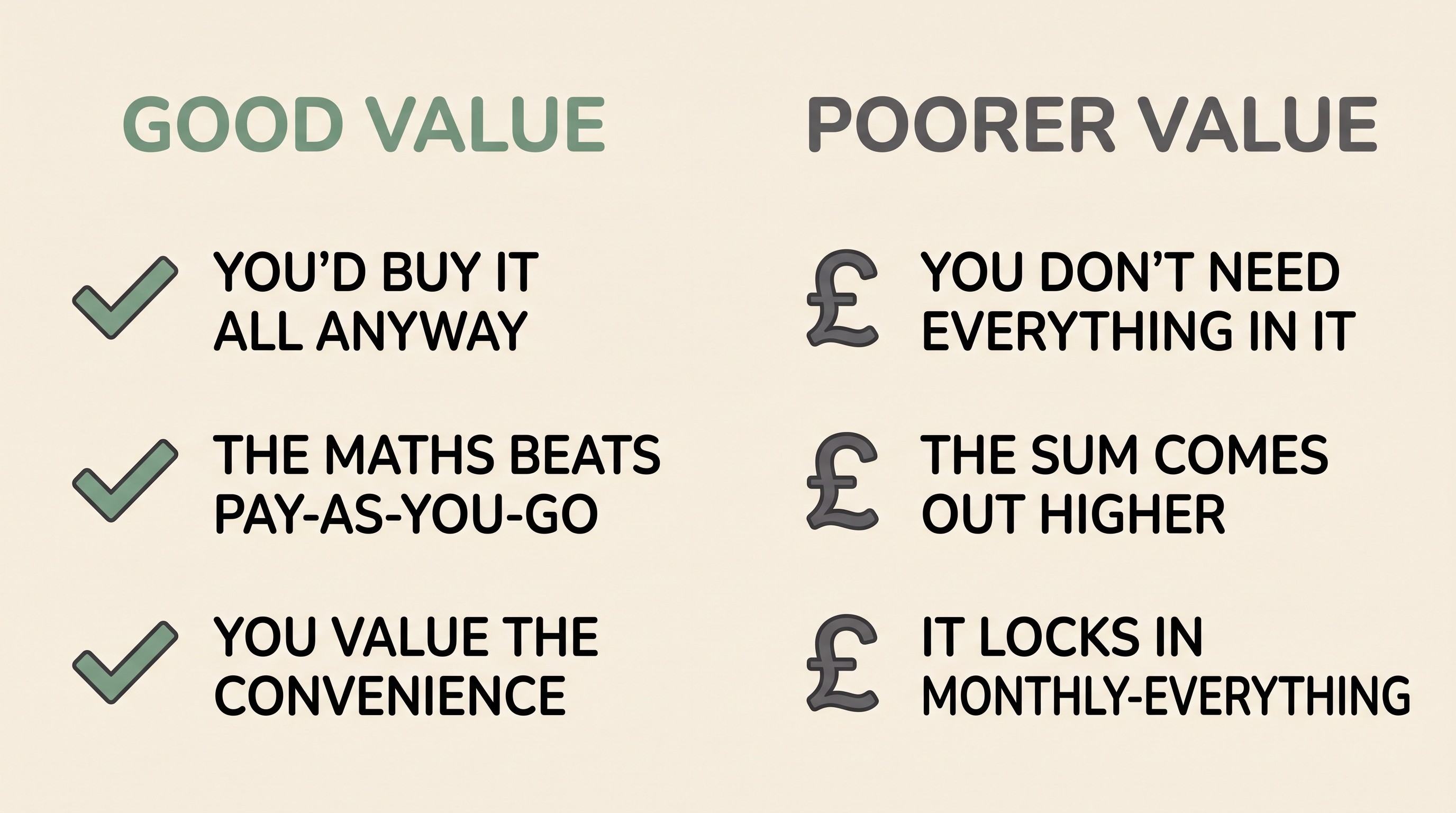

Step three: compare the two numbers. If the plan total is lower than the pay-as-you-go total for the things your pet actually needs, it's saving you money. If it's higher, you're paying a premium for convenience and for items your pet may not need.

The catch is in that last phrase. A plan is good value if your pet needs everything in it. It's poor value if you're paying for year-round monthly flea treatment your pet's lifestyle doesn't warrant, or worming at a frequency above what your pet's risk actually calls for. And that brings us to the bias.

The bias to factor in: plans are built around "monthly-everything"

Here's the honest part that the leaflet won't spell out, and we're going to say it plainly without attacking any practice.

Wellness plans are, by design, built around the maximum-treatment default: year-round, monthly flea and tick cover and frequent worming for every pet on the plan, regardless of that individual pet's actual risk. That default is convenient and it's simple to administer, but it's not what the profession's own current guidance recommends. The bodies that set the standards, the BVA, BSAVA and BVZS in their guidance on responsible use of parasiticides, now advise risk-assessing the individual animal and avoiding blanket, one-size-fits-all treatment (BVA/BSAVA/BVZS, 2021, updated 2025). ESCCAP, which guides worming in the UK, takes the same risk-based line rather than "monthly for everyone" (ESCCAP UK & Ireland).

So a plan can, without anyone intending anything sinister, quietly commit you to a level of parasite treatment above what your specific pet needs. For a dog that eats slugs in a lungworm hotspot, or a cat with a flea allergy, that intensive cover is exactly right and the plan is doing you a favour. For an indoor cat with no other pets and no risk factors, paying every month for year-round flea and worm product may be treating a risk that isn't really there.

This isn't a reason to distrust your vet. It's a reason to ask a better question: "does the treatment level in this plan match what my pet actually needs?" If it does, the plan is genuinely convenient. If it's more than your pet needs, you can ask whether the plan can be tailored, or whether pay-as-you-go on a risk-based schedule suits you better. Our pieces on whether your pet needs monthly flea treatment and how often to worm give you the vocabulary for that conversation, and the same logic applies to flea and worm subscription boxes, which share the identical monthly-everything design.

When a plan is genuinely good value

To be fair to a product that helps a lot of people, here's when signing up is the sensible call:

- Your pet genuinely needs everything in the bundle (real parasite risk, due vaccinations, the health checks).

- The maths comes out in your favour versus paying separately.

- You value the convenience and the discipline. If bundling means you never miss the flea treatment or skip the health check, that reliability has real worth, especially for a busy household.

- You'll use the discounts on things you'd buy regardless.

And here's when to pause and do the sum properly first:

- Your pet is low-risk and doesn't need the intensive parasite cover the plan defaults to.

- The annual total is higher than pay-as-you-go for what you'd actually use.

- You're joining mainly because it was offered at the desk, not because you've compared it.

The small print worth reading before you sign

The maths tells you whether a plan is good value on paper. The terms tell you whether it stays good value in practice, and this is where a bit of care pays off. Before you commit, ask the practice a few plain questions:

- Is there a minimum term, and what happens if I cancel? Some plans run on a rolling monthly basis, others tie you in for a year. A few operate so that if you leave partway through, you may owe the difference between what you've paid in and the value of the treatments you've already had that year, because the annual cost is spread rather than paid as you go. That's not a trap, but it's worth knowing before you sign, not after.

- What happens if I move house or change practice? Plans are usually tied to that specific practice or group. If you move, the plan generally doesn't move with you, so a plan makes most sense when you're settled.

- Is the flea and worm product on the plan a specific one, and does it suit my pet? The plan will supply whatever product the practice has chosen, which is fine if it fits your pet's needs, but it's worth confirming it covers the parasites your pet is actually at risk from (lungworm cover, for instance, isn't in every wormer).

- Are the health checks with a vet or a nurse, and does that matter to me? Both are valuable, but knowing which you're getting helps you judge the offer.

None of these should put you off a plan that suits you. They just stop the plan being a surprise later, which is the whole point of reading before you sign anything.

The honest bottom line, and your next step

A vet wellness plan is a convenience-and-budgeting product, not a con and not a must-have. It's genuinely good value when your pet needs what's in it and the maths works, and it's poor value when it commits you to more treatment than your pet's risk warrants. The single thing that tells you which camp you're in is the back-of-envelope sum, plus one honest question to your vet about whether the treatment level fits your individual pet.

So before you sign, or before your next renewal if you're already on one, do two things: run the twelve-month comparison, and ask your vet whether the parasite cover in the plan matches your pet's actual risk. If both come out in the plan's favour, join with confidence. If they don't, you now know exactly why, and you can build a right-sized preventive routine instead, which is what the Preventive Care Scheduler is for, holding your boosters, worming and health checks on the schedule your pet actually needs rather than a one-size-fits-all monthly default.

References

Keep track of how your pet is doing

The owners who cope best are the ones who notice changes early. A simple health log shows you what is working, and what is not, before the next vet visit.

Start tracking, freeYou're not doing this alone

Compare treatment journeys and talk to owners managing staying well. Free to join.

Join PetsLikeMine