Choosing Pet Insurance: A How-to-Choose Framework

Dr. Alastair Greenway

MRCVS

If you've ever tried to buy pet insurance, you'll know the feeling. Dozens of policies, a wall of jargon, premiums that range wildly for what looks like the same thing, and a nagging worry that you'll either pay over the odds or discover a fatal small-print gap at the exact moment your pet needs treating. It's genuinely hard, and most of the "help" out there is a comparison site that earns money when you click, which isn't the same as help.

So let's be straight about what this piece is, and what it isn't. This is a framework, not a recommendation. We don't name insurers, we don't run a price comparison, we don't take commission, and there are no affiliate links anywhere on this page. That's a deliberate choice, because the moment we start pointing you at a "best buy" we stop being honest brokers and start being a shop. What we're going to do instead is teach you how the policies actually work, so you can pick the right one for your pet yourself and see through the marketing while you're at it.

Why insurance even matters: the chronic-condition problem

Before the mechanics, it helps to understand what you're actually insuring against, because it changes which policy is right.

A one-off accident, a swallowed sock or a cut paw, is a bill you might grumble at but could probably absorb. The thing that genuinely ruins finances, and forces heartbreaking decisions, is the long-term condition. Arthritis, diabetes, allergies, heart disease, some cancers: these don't resolve in a fortnight. They can run for years, with repeat consultations, medication, and monitoring, and the bills add up to thousands over a pet's life.

Here's the key insight that the whole framework hangs on: the difference between policy types barely matters for a one-off, and matters enormously for a chronic illness. So as you read the four types below, keep asking one question: "what would this policy do if my pet developed something that lasted the rest of its life?" That's the scenario insurance exists for.

The four policy types, in plain English

Almost every pet policy on the market, however it's branded, is one of these four shapes. Learn the shapes and the marketing names stop mattering.

1. Lifetime. This is the most comprehensive, and usually the most expensive. It gives you a set amount of cover per year, and that amount refreshes every policy year for as long as you keep renewing without a break. So if your dog develops arthritis at four, a lifetime policy can keep contributing towards that arthritis every single year for the rest of its life, resetting the pot each year. This is the type built for the chronic-condition scenario.

2. Maximum-benefit (also called per-condition). You get a fixed pot of money per condition. Once you've claimed that full amount for, say, your cat's diabetes, that condition is done, exhausted, no more cover for it, even though you keep paying premiums and even though the diabetes obviously continues. It works fine until a long-term illness burns through the pot, which for a chronic condition it will.

3. Time-limited. You get cover for each condition for a set period only, commonly 12 months from when it first appears, and often a lower cash limit too. After that window closes, that condition becomes excluded, permanently. Cheaper premiums, but the cover switches off exactly when a long condition gets expensive.

4. Accident-only. The cheapest, and the narrowest. It covers injuries from accidents, and not illness at all. No cover for the diabetes, the lumps, the itchy skin, the dodgy heart. For some owners on a tight budget it's better than nothing, but understand that it excludes the entire category of illness that costs the most.

If you take one thing from this section: lifetime is the only one of the four that keeps paying towards a lifelong condition year after year. The other three all have a mechanism that switches off cover for a chronic illness, whether by exhausting a pot (max-benefit), closing a time window (time-limited), or excluding illness entirely (accident-only). That's not a scam, it's why they're cheaper. You're just choosing where the ceiling sits.

The concepts that catch people out

The policy type is half the story. The other half is a handful of terms that quietly decide whether you're actually covered when it matters.

Pre-existing conditions. This is the big one. No standard policy covers a condition your pet already has when you take the policy out, or often anything related to it. If your dog was treated for a limp last year, a brand-new policy may exclude that leg, that joint, or arthritis generally. This is why the worst possible time to shop for insurance on price is after a diagnosis, and why switching insurer to save a few pounds can quietly strip out cover for everything your pet has already had.

Per-condition vs overall limits. Some policies advertise a big total number but cap what they'll pay per condition underneath it. A headline "£10,000 of cover" can still leave you short if there's a lower per-condition sub-limit. Always read the per-condition figure, not just the shiny total.

The excess, and the co-payment. The excess is the fixed amount you pay towards each claim (or each condition per year). On top of that, many policies add a co-payment, a percentage of every bill you pay yourself. Crucially, that co-payment often rises as your pet gets older, sometimes kicking in at a set age and climbing from there. So a policy that looks affordable for a young pet can quietly hand you a growing share of every senior-years bill, which is exactly when the bills are biggest.

Why the cheap premium is cheap. When one quote is dramatically lower than another, it's almost never because that insurer is generous. It's usually because it's a time-limited or per-condition policy, has a high excess or co-payment, or has a low per-condition cap. Cheap isn't wrong, but it's cheap for a reason, and the reason is where the cover gets thinner.

The honest alternatives, presented without steering

Insurance isn't the only way to handle vet bills, and a good framework tells you the alternatives even though we're not selling any of them.

Self-insuring. Instead of paying premiums, you pay the same money into a dedicated savings pot every month and use it for vet bills. For a disciplined saver with a young, healthy pet, this can work well, and anything unspent stays yours. The risk is obvious: a serious illness in year two, before the pot has grown, can dwarf everything you've saved. It suits people who can genuinely ring-fence the money and top it up after a big claim.

The reality of rising premiums. Whichever route you choose, be clear-eyed that premiums rise as pets age, often steeply, because older pets claim more. A policy that's cheap for a puppy or kitten won't stay cheap, and budgeting only for today's premium sets you up for a shock. This isn't a reason to avoid insurance, it's a reason to factor the trajectory in from the start.

We're not going to tell you insurance beats saving, or the reverse. The right answer depends on your finances, your discipline, and your appetite for risk. What matters is that you choose knowingly rather than by default.

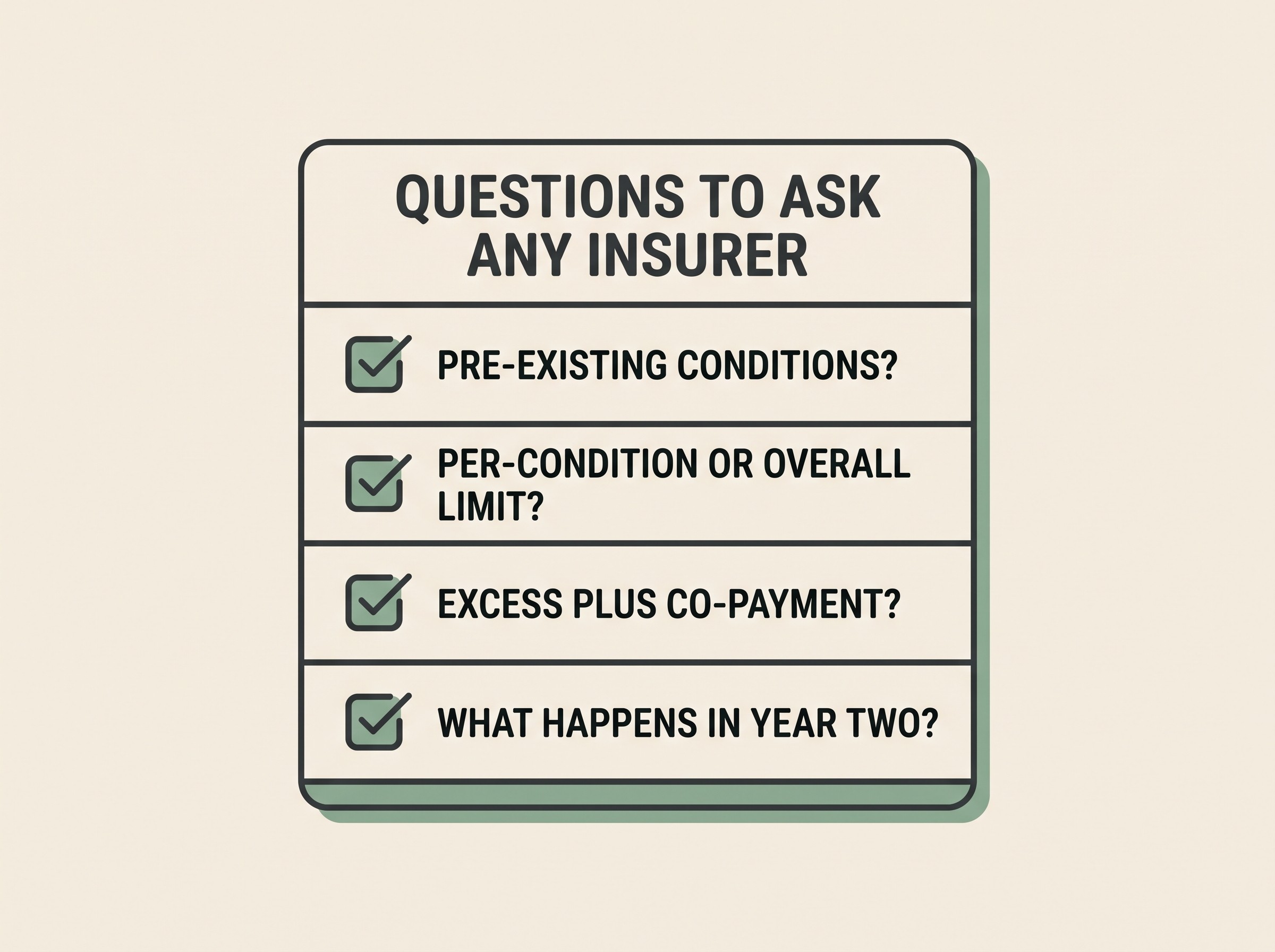

The questions to take to any provider

Here's the practical payoff. You don't need us to compare policies, because you can interrogate any of them yourself with a short list. Before you buy, get clear answers to these:

- Is this lifetime, max-benefit, time-limited, or accident-only? (Make them tell you the shape, not the brand name.)

- What's the limit per condition, per year, and overall? (All three, not just the headline.)

- What's the excess, and is there a co-payment percentage? (And does the co-payment rise with age?)

- What happens in year two and beyond for a condition that started in year one? (This is where time-limited and max-benefit reveal themselves.)

- What counts as pre-existing, and how far back do you look?

- Are dental, behavioural, complementary or prescription-diet costs covered, or excluded?

If a policy can't give you clean answers to those, that's your answer.

The one trap to avoid, and your next step

There's a single mistake that costs owners more than any other: shopping on price after a diagnosis, or switching insurer once your pet already has a condition. Because no policy covers a pre-existing condition, moving to a cheaper insurer after your pet develops, say, arthritis can leave that arthritis uncovered forever, even though it was covered under the old policy. The saving is an illusion that surfaces at the worst possible moment.

So the honest version of the advice is this. Choose your policy shape early, ideally while your pet is young and healthy, using the framework above. Then, once you're in a policy that fits, be very cautious about switching for a small saving. And whatever you choose, review it once a year at renewal, because that's when premiums jump and terms change. This is a natural fit for the Preventive Care Scheduler, which can hold an annual insurance-renewal review for you, so you actually read the renewal instead of letting it roll.

This framework helps you judge any policy against your own pet. If your pet already has a condition, tell any new insurer honestly and check exactly what's excluded before you move a single thing. And if what you're really weighing up is your vet practice's monthly plan rather than insurance, that's a different question with a different answer, covered in are vet wellness plans worth it?, because a wellness plan and an insurance policy do genuinely different jobs and it's easy to muddle them.

References

Keep track of how your pet is doing

The owners who cope best are the ones who notice changes early. A simple health log shows you what is working, and what is not, before the next vet visit.

Start tracking, freeYou're not doing this alone

Compare treatment journeys and talk to owners managing staying well. Free to join.

Join PetsLikeMine