Pet insurance for a new pet: lifetime vs annual, and why timing wins

Dr. Alastair Greenway

MRCVS

Of all the admin that lands on you with a new puppy or kitten, insurance is the one that feels the easiest to put off and is actually the most urgent. Not because something is about to go wrong, but because the choice you make in the first week or two quietly decides what will be covered for the rest of your pet's life. That's a big claim, so let me explain it properly, because most of the regret I hear about pet insurance comes from a decision that was made, or delayed, without anyone understanding how it works.

A word on what this is and isn't. I'm not here to sell you anything, or to point you at a particular company. I can't tell you which policy to buy, and neither can any other vet. What I can do is explain the different types of cover, the one timing rule that matters more than the premium, and the traps that catch people, so that you make the decision with your eyes open. We're explaining, not selling.

The honest case for insuring a young pet

Let's start with why to bother at all, honestly. Most weeks, most young animals are fine, and the premium can feel like money for nothing. The point of insurance isn't the likely week. It's the rare, expensive one.

A single orthopaedic surgery, a swallowed sock that needs removing from the gut, a serious illness that needs days of hospitalisation, any of these can run into thousands of pounds. That's the risk you're insuring against: not the routine, but the sudden bill big enough to force a choice no one wants to face, between their pet and their finances. Insurance turns that catastrophe into a manageable monthly cost. That's the whole deal, and for most families it's worth it.

It's also worth saying what insurance doesn't do. It doesn't usually cover routine, predictable costs like vaccinations, worming, flea treatment or neutering. Those are ordinary running costs to budget for separately (our guide to choosing a pet covers the wider cost picture). Insurance is for the unexpected.

The four types of cover, plainly

This is where a lot of people go wrong, because the policies look similar on a comparison site and behave completely differently when you claim. There are broadly four types in the UK, and the differences are the whole game.

Accident-only is the most basic and cheapest. It covers injuries from accidents, but typically not illness at all. Since a great many of the big bills in a pet's life come from illness, not accidents, this is usually the least useful for long-term peace of mind.

Time-limited cover pays for a condition for a set period, often twelve months from when it starts, after which that condition is generally excluded. It's cheaper, but it's a poor fit for anything that turns out to be long-term, because the cover runs out while the condition carries on.

Maximum-benefit (sometimes called per-condition) cover gives you a fixed pot of money per condition, with no time limit but no yearly reset. Once you've used the pot for a given condition, that's it for that condition, forever. It can work well for one-off problems and less well for a chronic one that keeps drawing on the same pot.

Lifetime cover is the most comprehensive, and usually the one I'd suggest people understand properly before dismissing on price. It gives you an amount of cover each year that refreshes at every renewal, for as long as you keep the policy going. That yearly reset is what makes it able to keep covering a long-term condition, year after year, for the life of the pet.

Why lifetime cover matters so much for a young pet

Here's the crucial point for a new owner. Many of the conditions that make insurance worth having are chronic: they don't get fixed and forgotten, they need managing for years. Arthritis, diabetes, some skin and allergy conditions, several heart and kidney diseases, all of these can mean ongoing costs across much of a pet's life.

Only lifetime cover is really built for that. With a time-limited or maximum-benefit policy, a chronic condition can exhaust its cover and then leave you paying out of pocket for the rest of the animal's life, often the most expensive stretch. With lifetime cover, the annual allowance refreshes each year, so a dog with arthritis or a cat with diabetes can keep being covered year after year. For a young animal with a long life ahead and, in some breeds, known predispositions, that's exactly the scenario worth protecting against. Look up your breed on its breed hub (swap in yours) to see what it's prone to, and you'll see why lifetime cover is often the sensible default for a pet whose whole life is still ahead of it.

The timing rule that matters most

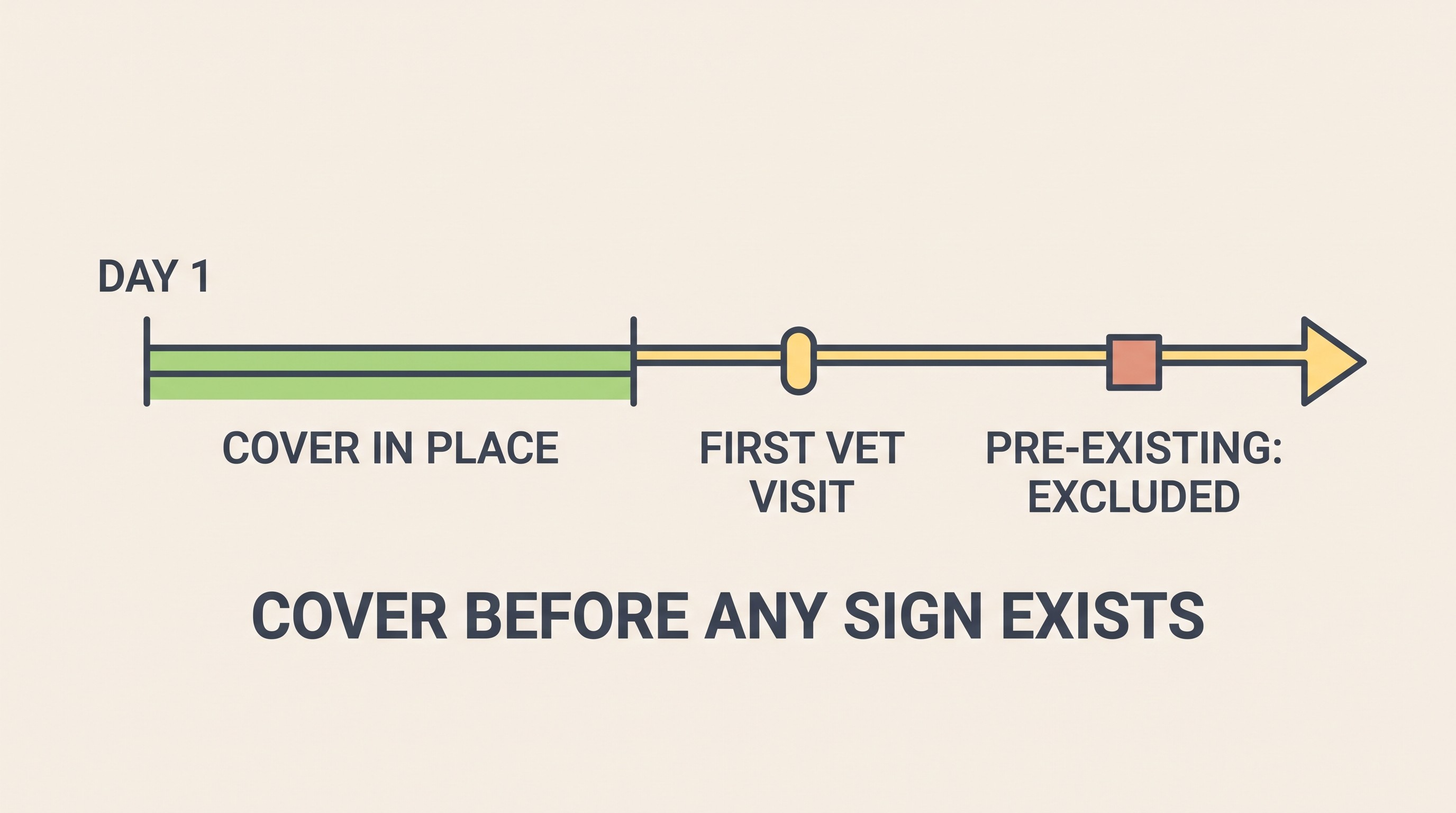

If you take one thing from this article, take this. Buy cover before any signs of a problem exist, because anything your vet has already noted becomes a pre-existing condition, and pre-existing conditions are excluded, very often permanently.

This is standard across UK insurers, and it's the single most consequential thing about the timing of your purchase. Insurance covers the unexpected. Once a condition, or even an early sign of one, is on the record, it's no longer unexpected from the insurer's point of view, so a policy bought afterwards won't cover it.

Play this forward and you see why day-one cover beats a cheaper policy bought later. Suppose you wait, and at the first vet visit your vet notes a slight heart murmur, or a bit of stiffness, or an itchy patch of skin. If you then take out a policy, that noted issue, and often anything related to it, is likely to be excluded for good. Whereas if the cover was already in place, it's covered. The few weeks you'd save by delaying can cost you cover for a whole category of problems for the rest of the animal's life.

So the practical rule is simple: get cover in place before the first vet visit if you possibly can. If your breeder or rescue gave you a few weeks of free introductory insurance, that's a helpful bridge, but note exactly when it ends and have your own policy ready to take over without a gap.

The traps worth knowing about

A few specific pitfalls catch people out, and they're all avoidable if you know them.

Switching insurer restarts pre-existing exclusions. If your pet develops a condition and you later move to a cheaper insurer, that condition will usually be treated as pre-existing by the new company and excluded. This is why chasing a lower premium each year can quietly strip cover from exactly the conditions you most need it for. Loyalty has a real value here that a comparison site won't show you.

Low annual limits that run out mid-treatment. A serious illness can outlast a small annual pot. Check that the limit is high enough to see a real course of treatment through, not just to look reassuring on the quote.

Per-condition caps. On maximum-benefit policies especially, a chronic condition can hit its ceiling and then leave you unfunded for the rest of the pet's life. Know whether your policy caps by condition, and whether that cap resets.

The alternative: self-insuring

There's an honest alternative for the financially disciplined: skip insurance and instead pay a set amount into a dedicated savings pot every month, so that you're building your own fund for a rainy day. In principle it can work, and for some people it does.

In practice, two things tend to undo it. The first is timing: a young animal can have a four-figure emergency in its first year, long before a savings pot is anywhere near big enough to cover it. The second is human nature: the pot gets raided for a holiday or a boiler, and the discipline slips. If you're genuinely certain you'll keep the money untouched and can absorb a large bill at any time, self-insuring is a legitimate choice. For most people, most of the time, insurance is the more reliable safety net precisely because it works from day one.

What your vet can and can't do here

Let me be clear about our role, because it's a common misunderstanding. Your vet cannot tell you which policy to buy, and shouldn't. What your vet can do is tell you what conditions your breed is prone to, so you understand what you're insuring against, and explain a diagnosis and treatment plan clearly so you can claim accurately. Beyond that, the choice of cover is yours, and the honest brokers of comparison are neutral sources like MoneyHelper or consumer bodies rather than any single insurer.

Your next step

Decide the type of cover now, before you get lost in premiums, and for most young pets that means seriously considering lifetime cover. Then put a policy in place before the first vet visit if you can, so nothing gets a chance to become pre-existing and excluded. If you were given introductory cover, diary the date it ends and line up your own policy to take over without a gap.

One last thing that pays off later: the record you're starting now makes future claims and vet conversations far easier. Keep every invoice and vaccination note, and let the lifetime record you build from day one do the remembering for you. When the first vet visit comes, our guide to what happens and what's legally required will help you make the most of it.

References

- General UK pet insurance practice: the four cover types (accident-only, time-limited, maximum-benefit, lifetime), premiums, excess and co-payment, pre-existing exclusions, and switching.

- Association of British Insurers (ABI): pet insurance definitions and market norms.

- PDSA PAW Report: UK pet ownership and cost figures, including typical treatment costs.

- Breed-specific predispositions: PetsLikeMine breed lens and `/breeds/<slug>` hubs. This article names no insurer and recommends no product. All insurance-practice statements are general and -flagged for confirmation against current UK terms at integration.

Keep track of how your pet is doing

The owners who cope best are the ones who notice changes early. A simple health log shows you what is working, and what is not, before the next vet visit.

Start tracking, freeYou're not doing this alone

Compare treatment journeys and talk to owners managing new puppy & kitten. Free to join.

Join PetsLikeMine