The Cost of Epilepsy and How Insurance Works

Dr. Alastair Greenway

MRCVS

Once the diagnosis lands and the panic of the first seizure fades, a more practical worry tends to follow: what is this going to cost us, for the rest of his life? It's a fair question, and an awkward one to ask out loud when your dog is the one who's unwell. So let me answer it plainly.

The single most important thing to understand is that epilepsy is rarely a course of treatment you finish. For most dogs and cats, idiopathic epilepsy means lifelong daily anti-seizure medication, because complete drug-free remission is uncommon (Bhatti et al., 2015). That sounds daunting, but the biggest cost is front-loaded and one-off, the ongoing costs are smaller and more predictable than people fear, and with the right insurance at the right time, most of it can be covered. This article owns the lifetime-cost picture; the detail of the tests lives in the diagnostic workup guide, and the ins and outs of each drug in the drugs compared guide.

One caveat before we start: every pound figure here is a practical estimate, not a peer-reviewed price. Costs vary enormously by region, practice and the size of your pet, so treat them as illustrative ranges and get real figures from your own vet. The clinical facts, by contrast, are cited and accurate.

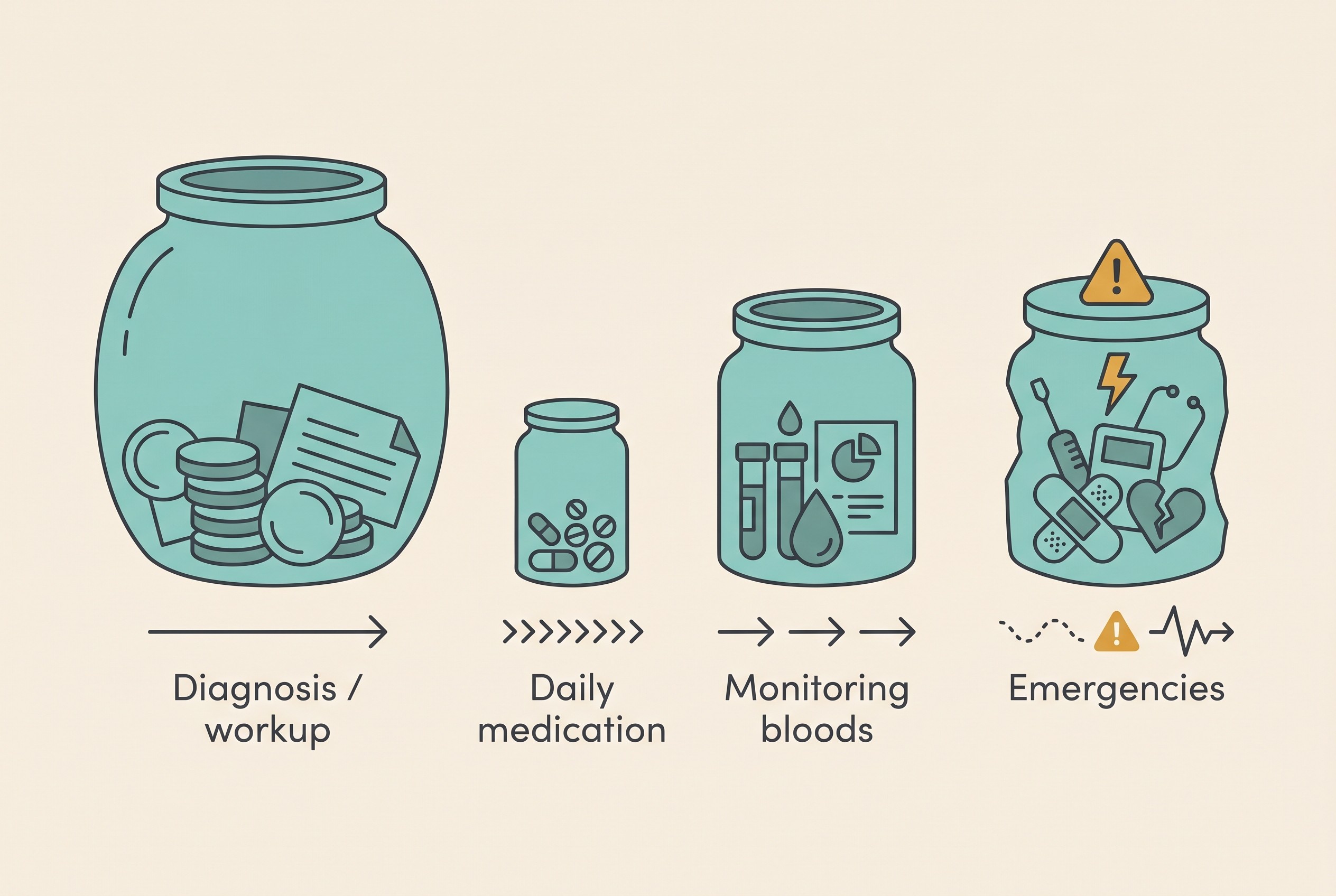

Where the money actually goes: four buckets

It helps to see "the cost of epilepsy" not as one number but as four things that behave very differently: a one-off diagnosis, the daily medication, recurring monitoring bloods, and unpredictable emergencies.

The diagnostic workup

This is the bill that makes people gasp. Confirming epilepsy properly can involve an MRI of the brain and a sample of the fluid around the spinal cord (CSF) under general anaesthetic, and that combination of advanced imaging plus anaesthetic time is genuinely expensive. One UK referral hospital lists a full seizure investigation at around £3,675, rising to roughly £3,938 with blood tests, with a neurology referral consultation alone at about £340 (Langford Vets, 2025), and independent UK estimates put the average dog MRI in the same broad bracket (NimbleFins, 2025). As a planning figure, expect the full workup to land around £2,000 to £4,000. The important nuance is that not every pet needs all of it: the workup is staged, and how far you go depends on your pet's age and exam findings. When an MRI genuinely earns its place is what the diagnostic workup guide is for; here, just know it's the front-loaded part.

Lifelong medication: the affordable surprise

This is the part that reassures most owners. The drug your vet is most likely to reach for first in dogs, phenobarbital (also written phenobarbitone, under brands like Epiphen or Phenoleptil), is favoured partly for its long history, wide availability and low cost (Bhatti et al., 2015). UK retail prices for Phenoleptil tablets run from around £0.16 for a 12.5mg tablet to about £0.71 for a 100mg tablet (VetUK, 2026), so a typical twice-daily regime often works out around £15 to £40 a month plus a dispensing fee, scaling with weight and dose. Set that against a four-figure workup and you can see why I call it the affordable bucket. One wrinkle: phenobarbital is a controlled drug in the UK, so it usually needs a posted hard-copy prescription rather than a quick online reorder. The other options (imepitoin/Pexion, levetiracetam/Keppra) cost more, but which drug suits your pet is a clinical decision, not a shopping one (see the drugs compared guide).

For cats, the drug set changes which costs apply: phenobarbital is first-line and levetiracetam the usual second choice, while potassium bromide is not used in cats at all and imepitoin (Pexion) isn't licensed for them, so neither cost applies to a feline budget. The insurance principles below apply to cats just the same.

Monitoring bloods

Some anti-seizure drugs need regular blood tests to use safely, a recurring cost you can plan for rather than dread. Phenobarbital and potassium bromide both need therapeutic drug monitoring, meaning blood-level checks alongside periodic general bloods, whereas imepitoin doesn't require level monitoring at all (Bhatti et al., 2015). The usual pattern for phenobarbital is a baseline panel before starting, then checks at around three months and roughly every six months thereafter (Bhatti et al., 2015). So budget for around twice-yearly blood tests for the life of treatment, more often early on and after any dose change, and ask your vet to bundle the drug-level check in with the routine bloods. The clinical why belongs in the drugs compared guide; here it's a predictable recurring line.

Emergencies

This is the bucket that justifies insurance. Most seizures, frightening as they are, are short and self-limiting and don't need an emergency dash. But three are genuine emergencies: a seizure lasting more than five minutes, two or more seizures in twenty-four hours, or seizures running into one another without recovery. Any of those means vet or emergency clinic now (Bhatti et al., 2015). For the budget, emergency admission, intravenous anti-seizure drugs, cooling and monitoring can run from hundreds into thousands of pounds per episode. For context, UK insurers paid out a record £1.23 billion in pet insurance claims in 2024, across 1.8 million claims, with an average claim of around £685 (ABI, 2025). An epileptic pet with a bad run of clusters is exactly the kind those figures are built from, which is the strongest argument both for cover and for prevention.

How UK pet insurance actually works for a lifelong condition

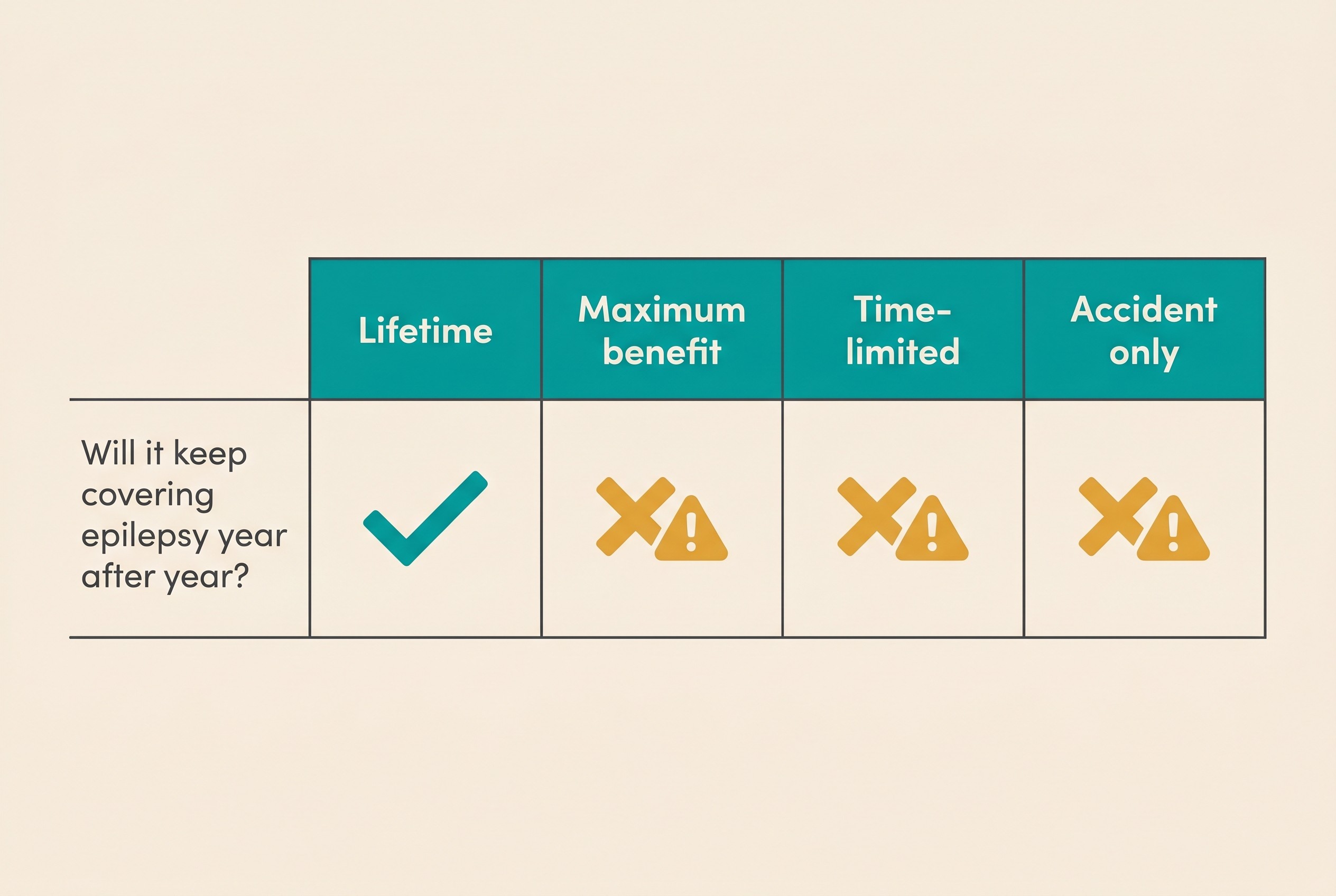

Here is where the choices you make genuinely change outcomes, because with a chronic condition the type of policy you hold matters more than almost anything else. There are four main kinds of UK pet insurance, far from equal for epilepsy (ABI, 2025; PDSA, 2025).

Lifetime policies are the only type that keeps paying for the same ongoing condition year after year. As the Association of British Insurers puts it, a long-term or recurring illness treated in one year will be covered again the next, with no limit to how many times, as long as the policy stays in force and payments are kept up to date (ABI, 2025). The annual limit resets at each renewal. This is the type epilepsy owners want.

Maximum benefit policies give you a fixed pot per condition. Once epilepsy has used up its limit, that condition won't be covered again, even after renewal (ABI, 2025), so for a lifelong condition the pot can run dry and the epilepsy is then uninsured.

Time-limited policies cover each condition only for a set period, typically twelve months from your first claim, after which that illness is no longer covered (ABI, 2025): unsuitable for epilepsy beyond the first year.

Accident-only policies are the cheapest because they cover accidents, not illness, so they do nothing for epilepsy.

The pre-existing trap, and why it matters most

Every UK insurer excludes pre-existing conditions, meaning anything that showed signs, was treated or was diagnosed before your policy started; most don't cover any pre-existing illness, so it's important to take out insurance as soon as possible (PDSA, 2025). For epilepsy that has two hard consequences.

First, insure before any signs ever appear. Once your pet has had its first seizure, getting new cover for epilepsy is very difficult: the condition will almost always be excluded from any new policy. The window is before it has ever shown itself, so insure a healthy young pet early and keep it going.

Second, switching insurer turns epilepsy into a pre-existing condition. If you change provider after diagnosis, you can lose cover for that condition, because the new insurer treats it as pre-existing (Which?, 2024); in one consumer review, only around 29% of dog policies were found to potentially cover any pre-existing conditions at all (Which?, 2024). So once epilepsy is diagnosed you're largely locked into your existing lifetime policy: when the premium rises at renewal, weigh that against losing the cover entirely. And you must declare known conditions when you apply or renew, or the policy can be voided (Which?, 2024).

Excess, co-payment and the annual limit

Three other features shape what you get back. There's usually a fixed excess per condition per policy year, and some policies, often on older pets, add a co-payment, a percentage of each claim on top (PDSA, 2025); with a lifelong condition both recur every year, so a cheap-looking policy can cost more in practice. The annual limit matters too: on a lifetime policy, epilepsy and any unrelated illness share the same yearly pot, so a limit set too low can be exhausted in a bad year.

Managing the cost without compromising care

None of this means resigning yourself to the worst-case bill, and none of it involves cutting clinical corners. Choosing a lifetime policy early is the highest-value move; beyond that, ask your vet and pharmacy about generic phenobarbital and the cheapest compliant way to fill a controlled-drug prescription, though which drug to use stays with your vet, never the price tag (Bhatti et al., 2015).

Above all, prevent the emergencies, because they're the priciest events. Give the medication reliably and on time, and never stop it abruptly, because withdrawal can itself trigger clusters or status (Bhatti et al., 2015). Our Seizure Diary is built for exactly this: logging frequency, spotting a worsening trend early and flagging when a cluster crosses into emergency territory, which can be the difference between a routine review and a costly night at the emergency clinic.

And if you're struggling, ask about help. Charities including the PDSA, Blue Cross and RSPCA offer subsidised or sometimes free care to those who qualify, and university teaching hospitals are often cheaper for an MRI than commercial referral centres (NimbleFins, 2025). It's also worth asking your practice about payment plans, or about settling a big one-off like the MRI directly with the insurer.

Is it worth it? A straight word on the long game

Behind the budgeting sits the real question: does all this cost and effort buy a good life? For most pets, yes. One community-based study found dogs with idiopathic epilepsy lived a median of 10.4 years from their first seizure, close to the general dog population, with no significant survival difference for those who had clusters or status (Hamamoto et al., 2016). A minority are harder to control, and those cases tend to be the more expensive ones, but for the majority cost and commitment buy good control. Plan for it, but don't let the frightening forum figure that clusters cut years off a dog's life make the decision feel hopeless: the better evidence doesn't support that as a rule (Hamamoto et al., 2016).

The most useful thing you can do today is get the insurance question right while you still can. If you're weighing up the tests, read the diagnostic workup guide; if treatment is on the table, the drugs compared guide shows where the medication costs really sit. And from day one, start logging in the Seizure Diary, because the cheapest seizure is the one you saw coming.

References

- Association of British Insurers (ABI). (2025). Types of pet insurance policy. Pet insurance guide.

- Association of British Insurers (ABI). (2025). Insurance payouts for "pawly" pets top £1 billion for third year in a row.

- Bhatti, S. A. H., De Risio, L., Muñana, K., Penderis, J., Stein, V. M., Tipold, A., et al. (2015). International Veterinary Epilepsy Task Force consensus proposal: medical treatment of canine epilepsy in Europe. BMC Veterinary Research, 11, 176.

- Hamamoto, Y., Hasegawa, D., Mizoguchi, S., et al. (2016). Retrospective epidemiological study of canine epilepsy in Japan using the International Veterinary Epilepsy Task Force classification 2015 (2003-2013): etiological distribution, risk factors, survival time, and lifespan. BMC Veterinary Research, 12, 248.

- Langford Vets (University of Bristol), Small Animal Referral Hospital. (2025). Neurology procedure prices.

- NimbleFins. (2025). Average cost of an MRI scan for a dog or cat.

- PDSA. (2025). Pet insurance guide.

- VetUK. (2026). Phenoleptil (phenobarbital) tablets for dogs, retail listing.

- Which?. (2024). Pet insurance explained.

Keep track of how your pet is doing

The owners who cope best are the ones who notice changes early. A simple health log shows you what is working, and what is not, before the next vet visit.

Start tracking, freeYou're not doing this alone

Compare treatment journeys and talk to owners managing epilepsy. Free to join.

Join PetsLikeMine