Funding Long-Term Arthritis Care: Insurance and Beyond

Claire Greenway

BVM&S MRCVS

Most owners put off reading anything about money until a bill forces the issue. I understand why. Money conversations are uncomfortable, the UK pet care funding landscape is genuinely complex, and the decisions you make about funding your dog or cat's chronic disease care will shape what's possible for them across the years ahead.

I want to help you make those decisions thoughtfully rather than reactively. That means understanding how UK owners actually fund pet care, what the genuine financial commitment of chronic disease management involves, the realistic options whether you're insured or not, and how to plan financially for the years of care ahead.

I'll be direct throughout. Veterinary care isn't cheap, and modern arthritis management costs real money. The owners who manage best financially are usually the ones who understood the picture clearly and planned accordingly, not the ones who hoped for the best and were surprised by the reality.

This article is written primarily for owners with newly diagnosed dogs or cats, but it applies equally to owners who've been managing arthritis for years and want to think more clearly about the funding side. Either way, the principles are the same.

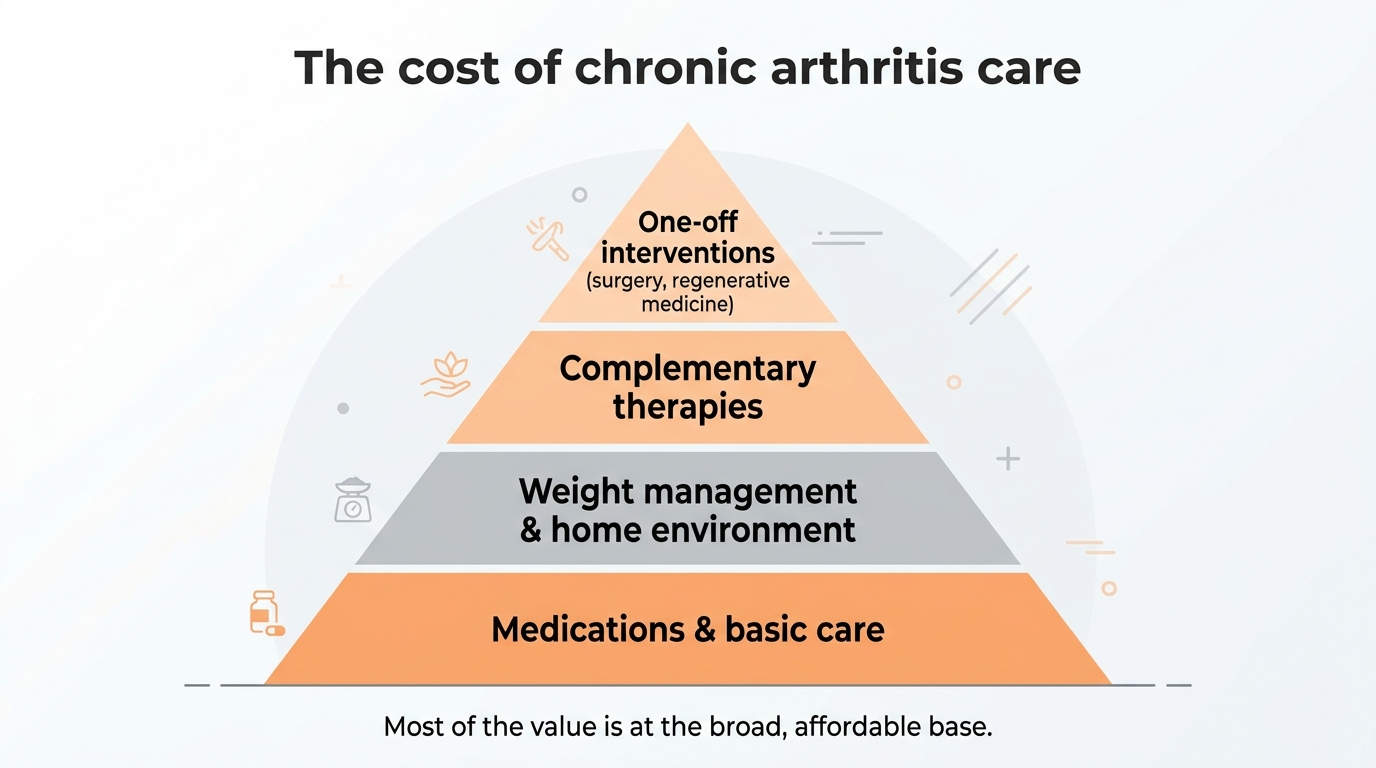

What you're actually budgeting for

Before we get into specifics, it helps to know what the spending actually looks like.

The cost of arthritis management varies enormously based on severity, the specific approach taken, and what your dog or cat individually needs. A reasonable mid-range estimate for ongoing care of a dog with moderate arthritis in the UK looks roughly like this:

Medications: £200-800 per year depending on which medications and at what doses. A typical NSAID regime is £150-400 annually; adding Librela injections takes this to £600-900; adding gabapentin or other adjunct medications adds £100-300.

Veterinary consultations: £200-500 per year for routine follow-ups, blood tests for medication monitoring, and the occasional unscheduled visit when something changes.

Hydrotherapy or physiotherapy: £1,000-2,500 per year for ongoing maintenance treatment. Less if used intermittently; more during active rehabilitation periods.

Acupuncture: £400-800 per year for maintenance treatment at typical UK rates.

Therapeutic joint diet or supplements: £300-600 per year for prescription joint food, or £200-400 for quality supplements added to standard food.

Home equipment and modifications: £100-300 per year as needs evolve (replacing beds, adding ramps, upgrading grip surfaces, etc.).

Total annual cost range for ongoing canine arthritis management: £2,000-5,500 per year for moderate cases, more for complex or severe ones.

For cats, the figures are somewhat lower but still meaningful. Solensia at £35-65 per monthly injection adds £420-780 annually if used. Cat-specific therapeutic diets and home modifications add similar proportional costs. A typical annual cost range for feline arthritis management is £1,000-3,500 per year.

These numbers don't include one-off costs that may arise: surgery (£3,000-10,000+ for major orthopaedic procedures), regenerative medicine (£3,000-8,000 for stem cell programmes), specialist referrals (£500-2,000 for initial workup), or emergency care during flare-ups.

Over a typical 5-8 year management period, total spending on a dog with arthritis can easily reach £15,000-40,000, with some cases significantly higher. For cats, £8,000-20,000 is realistic over the same period.

These are large numbers, and they're also the reality. The owners who manage best are the ones who plan for these costs rather than being surprised by them.

How UK owners actually pay for pet care

Before getting into insurance specifics, it's worth being candid about the funding landscape, because the picture isn't what veterinary professionals often assume.

There are around 38 million pets in UK households, including roughly 12 million dogs and 11 million cats. The Association of British Insurers reports around 4 to 5 million active pet insurance policies, depending on the year. That means insurance covers roughly one in five UK dogs and cats. For the other four in five, insurance isn't part of the picture at all.

This matters because most veterinary discussion of funding chronic disease care assumes insurance is the primary mechanism. In reality, insured owners are a minority. The majority of UK pet owners fund veterinary care through some combination of:

Direct payment from household budget. Most common by a significant margin. Owners pay practice bills as they arise from monthly income, often with modest stretching during particularly expensive months.

Dedicated savings. Some owners set aside money specifically for veterinary care, treating it as a planned expense rather than insurance premium.

Payment plans with veterinary practices. Many practices offer staged payment arrangements for established clients facing larger bills.

Credit when necessary. Personal loans, credit cards, or veterinary-specific financing for unexpectedly large costs.

Going without certain interventions. Owners declining specific treatments because of cost. This happens more than veterinary professionals often acknowledge.

Charity support for those eligible. Means-tested charities provide free or subsidised care for owners receiving qualifying benefits.

Insured owners tend to be over-represented in veterinary conversations because they're the ones spending the most through structured channels. The uninsured majority funds care more quietly, often making harder trade-offs, often with less visibility in the system. Most pet care funding content is written around insurance, which doesn't reflect how most UK owners actually pay for things.

If you're insured, the insurance section below matters most for you. If you're not, the practical sections on charity support, payment plans, self-insurance, and treatment prioritisation are where the genuinely useful content sits. Both groups should read both sections, because circumstances change and the considerations interact.

UK pet insurance: how it actually works (for the minority who have it)

For the owners who do have pet insurance, understanding how it works (and doesn't work) is essential for getting the value you're paying for.

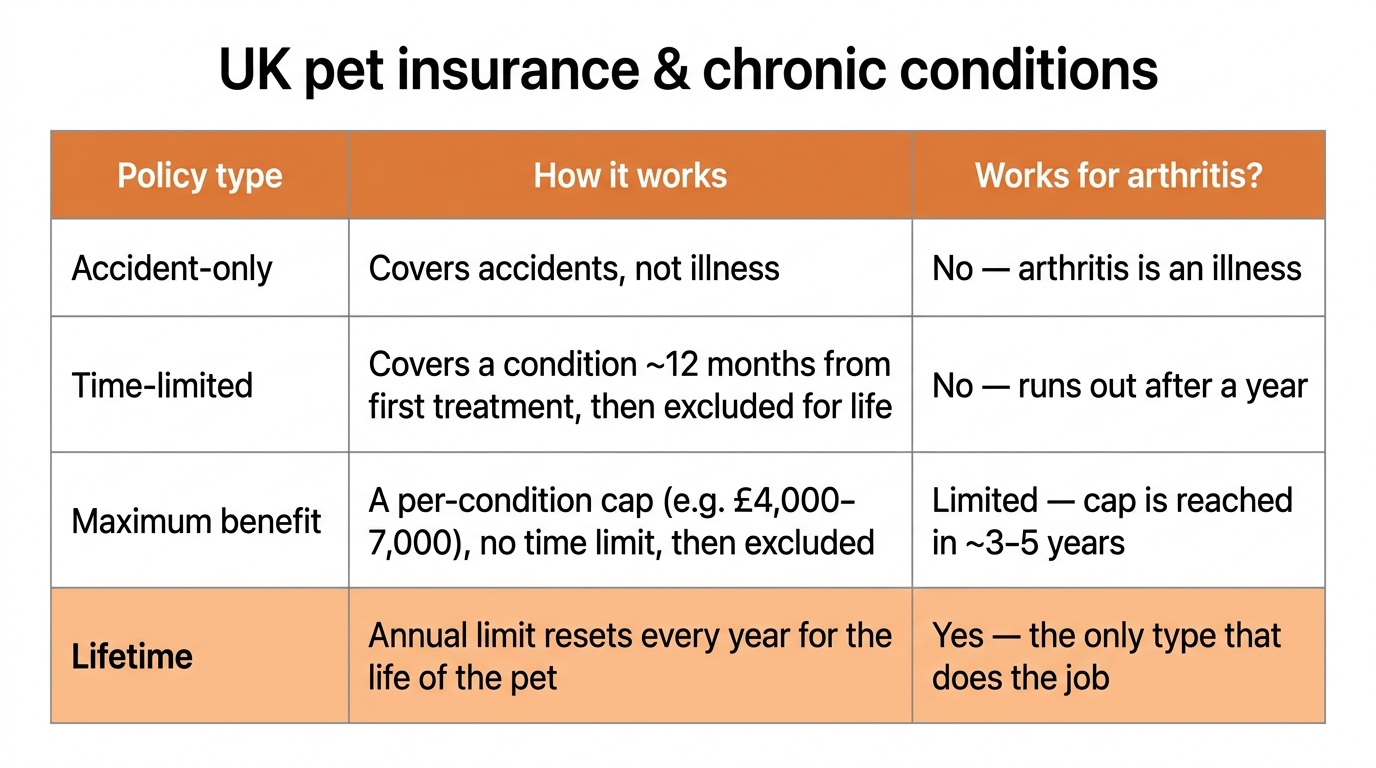

The four main policy types

Pet insurance policies in the UK fall into four broad categories, with significant differences in how they handle chronic conditions like arthritis.

Accident-only. The cheapest option. Covers only accidents, not illness. Useless for arthritis management because arthritis is an illness, not an accident.

Time-limited. Covers each condition for a defined period (typically 12 months) from when treatment first starts. After 12 months, that condition becomes excluded forever. For a chronic condition like arthritis, this means you have one year of cover and then you're funding it entirely yourself for the rest of the dog or cat's life. Time-limited policies are dangerous for chronic disease management.

Maximum benefit (per-condition limit). Covers each condition up to a maximum amount (e.g., £4,000 or £7,000) with no time limit. Once that maximum is reached for a specific condition, that condition is excluded from further claims. For arthritis where lifetime spending can easily exceed £20,000, the maximum is often reached within 3-5 years.

Lifetime cover. The annual limit resets each year, providing continuous cover for chronic conditions such as diabetes, epilepsy, or arthritis for the life of the pet, as long as the policy is renewed without break. In contrast, time-limited plans stop payments exactly 365 days after the first treatment date, forcing the owner to bear all future veterinary expenses themselves.

For chronic conditions like arthritis, lifetime cover is functionally the only insurance type that does the job. The others all fail in predictable ways at predictable times.

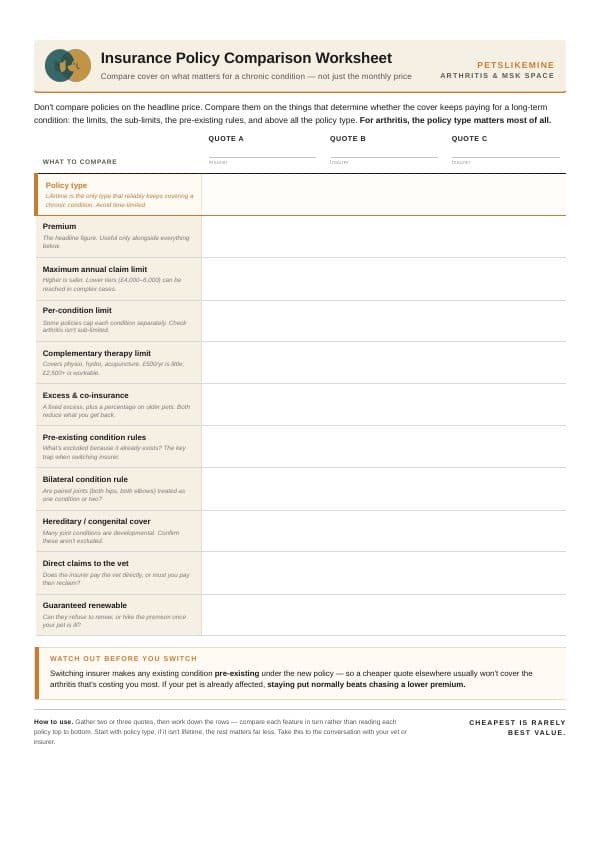

If you're comparing quotes, our insurance comparison worksheet lists the questions that matter for a chronic condition: per-condition limits, excess structure, the small print on continuing conditions, and what changes at renewal. Print it and use it on whichever insurer's site you're on.

What lifetime cover actually costs

UK lifetime pet insurance premiums vary based on breed, age, location, and the specific cover level. Indicative figures for 2025-2026: average monthly premiums in the UK for lifetime policies are roughly £35 to £55 per month for dogs (higher for large breeds or pedigree dogs). Cats are typically £15-30 per month for lifetime cover.

These are insurance starting prices. The critical thing to understand is how they change over time.

Premium escalation. Premiums rise as your pet ages, often substantially. By the time a dog is 10-12, lifetime cover premiums can easily be £80-150 per month for the same policy that was £35 at the start. This is one of the genuine downsides of lifetime cover that owners often discover late.

Claims history loading. Once you've claimed for a chronic condition, your premium often rises further at renewal. Some insurers apply specific loadings; others build it into general premium increases. Either way, the price you pay tends to climb most steeply for exactly the pets whose owners can least afford to switch away.

Total cost over a pet's lifetime. A lifetime policy on a dog from puppy through to 13-14 years might cost £8,000-15,000 in total premiums. For pets who develop significant chronic conditions, the policy pays out substantially more than this. For pets who stay healthy, the insurer profits. That's the basic insurance bargain.

The pre-existing conditions trap

When you switch insurers, every condition your pet has ever been treated for or shown signs of becomes pre-existing under the new policy. Conditions that were covered by your previous insurer often will not be covered by the new one. This is an important point to understand when comparing renewal quotes. The new policy is cheaper because it doesn't cover the chronic condition your pet developed under the old one.

If your dog develops arthritis while insured with Company A, and you stay with Company A, the arthritis remains covered as long as you keep paying premiums. If you switch to Company B because Company A's renewal price increased, the arthritis becomes pre-existing for Company B and is excluded permanently. You've now lost cover for the condition that's costing you the most.

This is why most owners with chronically ill pets stay put rather than chase price. The cheaper alternative isn't actually cheaper once you account for the lost cover. The strongest proof is a clean veterinary record over the insurer's symptom-free period combined with a written statement from your vet confirming the condition has fully resolved. Some insurers will lift pre-existing exclusions after 2-3 symptom-free years, but for chronic progressive conditions like arthritis, that symptom-free period essentially never arrives.

Gaps that remain even with lifetime cover

Even with lifetime cover, there are gaps owners should understand:

Sub-limits on specific treatments. Many policies have specific caps for complementary therapies (physiotherapy, hydrotherapy, acupuncture), often £500-2,000 per year. For a dog needing weekly hydrotherapy at £40 per session, that's £2,080 a year before the policy starts paying nothing.

Excess and co-insurance. Standard policies have an excess (typically £75-200) per condition per policy year, sometimes plus a percentage co-insurance (often 10-20%) for older pets. These add up significantly for high-claim chronic conditions.

Maximum annual claim limits. Even lifetime cover has annual limits. Lower-tier policies cap at £4,000-6,000 per year; higher-tier policies at £10,000-25,000 per year. For complex cases with multiple interventions, the lower limits can be reached.

Pre-existing exclusions on conditions present before policy started. Even lifetime cover doesn't help with conditions that existed before you took out the policy; those are still excluded.

Specific treatment exclusions. Many policies exclude or limit certain treatments: behavioural work, dental disease, alternative therapies in some cases. Read the policy documents.

Excluded breeds or breed-specific conditions. Some breed-related conditions (hip dysplasia in certain breeds, cruciate disease in others) may have specific exclusions or higher excesses.

When to insure

The straight answer is: as early as possible.

The ideal moment is when your pet is young and healthy, before any conditions have manifested. Insurance at this stage is cheaper, simpler, and ensures broad cover for whatever develops later.

For owners who didn't insure early and whose pet has now developed arthritis or other chronic conditions, the options are narrower. You can still get insurance, but the arthritis itself will be excluded as pre-existing. Cover for new conditions remains valuable but the major spend you're facing isn't covered.

For owners insuring an older pet who is currently healthy, getting cover before any conditions develop is still worthwhile. Premiums are higher than for puppies but you're still buying continuous cover for future problems.

The mistake most owners make is delaying. Dog insurance UK is one of those topics we often put off thinking about until it's urgent. The trouble is, by the time you need it, it's often too late to get the right cover.

Reading a pet insurance policy properly

Before committing to a policy, look beyond the headline price.

What to check specifically

Maximum annual claim limit. What's the total you can claim per policy year? Lower limits seem fine when premiums are cheap but fail at the worst moment.

Per-condition limits within the annual cap. Some policies have a maximum per condition that's lower than the annual cap. For arthritis cases needing comprehensive care, this matters.

Complementary therapy sub-limits. Specifically check the limit for physiotherapy, hydrotherapy, acupuncture. £500/year is essentially useless for chronic disease; £2,500/year is workable; £5,000/year is generous.

The excess and co-insurance structure. What do you pay before insurance kicks in, and what percentage of remaining costs do you cover?

Renewal terms. Can the insurer refuse renewal? Can they impose new exclusions at renewal? Some policies are guaranteed renewable; others aren't.

Bilateral condition rules. For conditions affecting paired structures (both knees, both hips, both elbows), how does the policy treat the two sides? Some treat bilateral problems as one condition; others as two. This matters significantly for cruciate disease where a significant proportion of dogs go on to rupture the cruciate on the other side within the following year or two.

Hereditary and congenital condition cover. Hip dysplasia, elbow dysplasia, patellar luxation: is breed-related arthritis covered?

Pre-existing condition definitions. How does the policy define pre-existing? Some are stricter than others. Has your pet ever shown any sign of the condition before policy start?

Specialist referral cover. Are referrals to specialists covered, including specialist costs that are typically much higher than general practice?

Treatment exclusions. What specific treatments aren't covered? Behavioural work, alternative therapies, dental, certain regenerative treatments.

Direct claims processing

Worth asking specifically: does the insurer process claims directly with veterinary practices, or do you pay upfront and claim back?

For chronic conditions with significant ongoing costs, direct claims processing is genuinely valuable. Paying £400 for hydrotherapy each month and waiting weeks to be reimbursed creates significant cash flow pressure that many owners don't anticipate.

Major specialist centres typically have direct claim arrangements with the larger insurers. General practices vary considerably. Confirm what your practice's arrangement is before committing to a policy.

Funding without insurance: the realistic picture for most owners

If you're one of the four in five UK dog and cat owners without pet insurance, the principles here aren't second-best; they're the realistic approach to chronic disease management for the majority of UK pet owners.

The single biggest mistake uninsured owners make is treating funding as something to figure out when bills arrive. The owners who do best plan in advance, build buffers, prioritise carefully, and communicate openly with their veterinary team about constraints. This is achievable. It just requires deliberate thought rather than reaction.

Self-insurance: the disciplined approach

For uninsured owners, the most effective approach is to treat veterinary care as a planned expense. Set up a dedicated savings account or pot specifically for veterinary costs. Contribute to it monthly with the discipline you'd give an insurance premium. Use it when needed.

The maths often works out favourably. £80 per month in dedicated savings is £960 per year. Over five years that's £4,800. For pets who don't develop major conditions, the money stays yours rather than going to an insurer's reserve. For pets who do develop conditions, you have a substantial buffer to draw on.

For owners specifically managing arthritis without insurance, a reasonable monthly contribution given the typical annual costs we covered earlier would be:

Conservative budget: £50-80 per month (£600-960 annually). Covers basic medication, routine vet visits, modest complementary therapy. Sufficient for foundational management.

Mid-range budget: £100-200 per month (£1,200-2,400 annually). Adds room for regular hydrotherapy or physiotherapy, occasional flare-up management, periodic specialist consultation.

Full budget: £250-400 per month (£3,000-4,800 annually). Approximates what insured owners often pay in premiums and excess combined. Allows full multimodal management.

The discipline is the same as paying insurance premiums. The difference is that the money stays yours, the rules are yours to set, and there are no pre-existing exclusions to worry about. The downside is that you bear the risk of large unexpected costs that insurance would have covered.

Many owners find that disciplined self-insurance combined with limited insurance cover (perhaps for emergency or accident-only) provides a workable middle ground.

Charity support for owners in genuine hardship

For owners receiving qualifying benefits, several UK charities provide subsidised or free veterinary care. These services have specific eligibility criteria and can't help every owner who's financially stretched, but for those who qualify, they're genuinely valuable.

PDSA (People's Dispensary for Sick Animals). The UK's largest veterinary charity, with around 48 Pet Hospitals across England, Scotland, Wales and Northern Ireland. The PDSA focuses on providing veterinary treatment to animals when their owners face severe financial hardship. Eligibility requires receiving certain qualifying benefits (Universal Credit, Housing Benefit, Pension Credit, and others depending on circumstances) and living within the catchment area of one of the Pet Hospitals. Eligible households can register exactly one pet for completely free treatment under current rules. For owners outside hospital catchments but still receiving qualifying benefits, the PDSA offers a Pet Care Scheme for subsidised services at a modest monthly cost. Check the PDSA website for current eligibility criteria and pricing.

Blue Cross. Operates a network of animal hospitals providing free or discounted veterinary care to eligible owners. Band A means the Blue Cross will fund veterinary treatment for two of your pets. To qualify for Band A you must be receiving certain benefits including Universal Credit (without reduction due to work or other income). Band B means the Blue Cross will provide veterinary treatment at a discounted rate. Eligibility depends on receiving qualifying benefits and living within service catchment areas.

RSPCA. Some regional branches offer veterinary care assistance, voucher schemes, or other financial support. Coverage varies significantly by area. The RSPCA offers services at a lower cost in certain parts of England and Wales. Check your local branch directly for what's available.

Regional and specialist charities. USPCA offers discounted veterinary treatment at their hospital in Newry, Northern Ireland. SSPCA provides some discounted veterinary services, such as neutering, in parts of Scotland. Dogs Trust's Hope Project provides help for pet owners who don't have a permanent residence. Cats Protection offers a means-tested neutering service for cats.

Eligibility for charity support is strict. Most require receipt of specific qualifying benefits and don't help owners who are simply experiencing temporary financial difficulty. If you think you might qualify, the PDSA Eligibility Checker on their website is the quickest way to find out what's available in your area. If you don't qualify but are facing genuine financial pressure, the practice-based options below become more important.

Payment plans and credit options

Most UK veterinary practices offer payment plan arrangements for owners facing significant treatment costs they can't pay upfront. The terms vary considerably:

Practice-direct payment plans. Many practices spread costs over 3-6 months interest-free for established clients. This is particularly common for surgical procedures with predictable costs. The relationship matters here; clients with years of straightforward history tend to be offered more flexible arrangements than new clients.

Third-party veterinary financing. Several companies offer veterinary-specific financing, often spread over 12-24 months with interest. Useful for larger one-off costs (£3,000+ surgery for instance) but adds total cost through interest.

Care Credit and similar consumer credit. Some consumer credit products are specifically designed for medical and veterinary care, with promotional periods (often 0% for 6-12 months) and longer-term financing options.

Personal credit (loans, cards). Useful in emergencies but expensive over time if not repaid quickly. Best used as a bridge to bigger purchases or while waiting for other funding (savings building up, insurance claims processing).

The practical advice: discuss payment options with your practice before you need them, not when you're standing at reception facing a bill. Most practices respond well to owners who communicate proactively about financial constraints, especially established clients with good histories. Some build payment plans into their standard offering for chronic disease patients.

When neither insurance nor charity nor savings is enough

There are situations where the funds genuinely aren't there. Either accumulated savings haven't reached the point where they cover what's needed, or income simply doesn't allow the contributions, or unexpected costs have outpaced planning.

When this happens, the practical options narrow:

Have the difficult conversation with your vet. Be straight about what you can and can't afford. Ask for the cheapest reasonable approach to managing your pet's condition. A good vet will work with you to find an acceptable path.

Prioritise pain management above everything else. A dog or cat in unmanaged chronic pain has poor welfare regardless of what else is happening. Pain control should be the last thing you sacrifice on.

Consider whether your treatment plan can be simplified. Multimodal management is ideal but isn't the only option. Sometimes simplifying to fewer interventions (just medication and weight management, for instance) is the realistic choice and still produces acceptable outcomes.

Accept that some interventions won't happen. Hydrotherapy is great, but if you can't afford it, you can't afford it. Make peace with that and focus on what's possible. Many dogs and cats live good lives on basic management alone.

Be willing to talk about end-of-life options early. If the financial situation makes adequate care genuinely unsustainable, and your pet's quality of life is suffering as a result, that's a conversation worth having sooner rather than later. Some of the most thoughtful owners I see are those who make difficult decisions about timing rather than letting the financial pressure produce worse outcomes for everyone.

Pretending the financial reality doesn't shape welfare decisions doesn't help anyone. A frank conversation about what's possible serves your pet better than hoping the money will materialise.

Prioritising care within budget constraints

When funds are limited, treatment prioritisation becomes important. The principles I'd suggest:

Pain management first. Adequate pain control is the most important intervention. A dog or cat in significant pain has poor quality of life regardless of what else you're doing. NSAIDs at correct doses are typically the cheapest effective option (£150-400 per year) and should be the foundation.

Weight management second. Often free or very cheap. Significant impact on arthritis. Eliminating excess weight reduces medication needs and joint loading simultaneously.

Environmental modification third. One-off costs in the £200-500 range usually. Significant impact on daily comfort. Worth doing early.

Quality nutrition fourth. Affordable upgrade from cheapest food to mid-range quality food with appropriate protein and omega-3 content. Typically £200-400 per year above standard food costs.

Selective complementary therapies fifth. Hydrotherapy if affordable, acupuncture if appropriate for the case, physiotherapy if needed. These add cost but produce meaningful benefit.

Expensive interventions last. Stem cell therapy, complex surgery, monthly biologics like Librela or Solensia are valuable but not essential first-line treatments. Many dogs and cats do well without them.

The reality is that you can manage canine arthritis reasonably well for £600-1,200 per year if you focus on the foundations and skip the expensive add-ons. Not optimally, but reasonably. For owners with genuine financial constraints, this matters.

Decision scenarios

A few specific scenarios worth thinking about across the insured/uninsured spectrum.

You're getting a new puppy or kitten

If you can afford lifetime cover, this is the moment when it makes most sense. Premiums are lowest, no conditions exist yet to exclude, and you're buying decades of potential cover. Insure them immediately, before bringing them home if possible.

For breeds prone to specific conditions (Labradors with hip dysplasia, French Bulldogs with multiple conditions, Maine Coons with hip dysplasia), insurance is particularly important and getting it before any breed-related conditions manifest is critical.

If lifetime cover isn't affordable, start a dedicated veterinary savings pot immediately and contribute monthly. Even modest contributions from puppy age build meaningful buffers over the years.

Your pet is older but currently healthy

If you have lifetime cover already, keep it. The premium escalation is annoying but the protection against future major conditions becomes more valuable as your pet ages.

If you don't have insurance, the value calculation is different. Premiums for older pets are higher and the years of cover ahead are fewer. Run the maths on expected premiums versus realistic future costs. For some older but healthy pets, insurance is still a good deal. For others, dedicated savings may be more efficient. The decision is genuinely closer than it is for younger pets.

Your pet has just been diagnosed with arthritis

The arthritis itself is now pre-existing for any new insurance policy. The options:

-

If you have lifetime cover, stay with the current insurer. Switching now will make the arthritis pre-existing for any new policy. This is the single most important decision you'll make.

-

If you have time-limited or maximum benefit cover, understand its limits. Your cover for arthritis will probably end at the 12-month mark or when the per-condition limit is reached. Plan for the funding transition that follows.

-

If you have no cover, don't try to take out new cover for the arthritis. It will be excluded. Consider lifetime cover for other potential future conditions, or focus on disciplined self-insurance.

-

Regardless of insurance status, build the savings pot. Insurance excess, sub-limit overruns, and out-of-pocket costs all benefit from having buffer money available.

The worst outcome is dropping useful insurance because the arthritis isn't covered any more. Other conditions will likely emerge over the years; cover for those still has value.

Your pet has multiple chronic conditions

The financial picture is challenging regardless of insurance status. For insured owners, the annual cover limits are being stretched. For uninsured owners, the monthly costs are higher and the buffer harder to maintain.

For owners in this position, the priorities are the same:

- Use any existing cover to its maximum allowance each year

- Apply for charity support if eligible

- Discuss payment plans proactively with your veterinary team

- Prioritise treatments by benefit per pound rather than aspiration

- Have frank conversations within the family about the budget reality

This is uncomfortable but it's the reality. Clear-eyed financial planning beats hoping for the best.

Talking money with your veterinary team

Money conversations with your vet are sometimes awkward but they're essential.

What to tell your vet

Your budget situation, plainly. Not what you wish you could afford, but what you actually can. Vets adjust their recommendations to match what's feasible.

Your insurance situation. What's covered, what isn't, what the limits are.

Your priorities. Pain control above all? Maximum quality of life regardless of cost? Practical balance?

What to ask

What are the priorities for spending? What produces the most benefit per pound for your specific dog or cat?

What can wait? Some interventions are clearly important now; others can be delayed without harm.

What's the cheapest reasonable option? Not "the cheapest" but "the cheapest that's still reasonable medicine."

What would you do if this were your own pet, and your budget were similar? A direct question that often produces candid answers.

Can we do this in stages? Spreading costs across months rather than all at once.

Good vets respond to frank financial conversations with practical guidance. Bad ones don't, in which case the relationship may not be right for chronic disease management.

Planning for the long view

Some practical principles for thinking about the financial dimension across years.

Track actual costs. Spend a year noting what you actually pay for vet care. The total often surprises owners who haven't tracked it. This is genuinely useful data for planning.

Anticipate phase changes. Arthritis management costs typically rise over time as more interventions become appropriate. Year one might cost £1,500; year five might cost £4,000. Plan for this trajectory.

Build a buffer. Even insured owners benefit from having £500-2,000 in dedicated savings for excess payments, sub-limit overruns, and one-off costs.

Communicate within the family. Whoever else is involved in the household finances needs to be on the same page about what's being spent and why. Surprises create stress that affects everyone.

Don't make purely emotional decisions in crisis. Decisions about surgery, expensive treatments, or end-of-life care are easier when the financial framework has been thought through in advance, before the emotional pressure of the moment.

Be willing to talk about end-of-life decisions when finances become unsustainable. This is the hardest conversation. Sometimes the kindest decision is the financially sustainable one rather than the most aggressive one. We address this in our quality of life article.

A final thought

The financial dimension of chronic disease care isn't separate from the clinical dimension. The two are interwoven, and they affect each other constantly. A treatment plan that's financially unsustainable will fail. A purely financial decision that ignores quality of life will hurt your dog or cat. The goal is to balance both carefully.

The owners I see managing best aren't the wealthiest. They're the ones who've thought clearly about both the clinical needs and the financial reality, made decisions that align the two, and built sustainable patterns of care that they can maintain across the years.

Money in pet care is uncomfortable. But ignoring the financial dimension doesn't make it go away. It just means you make worse decisions when you're forced to face it later, under pressure, with less time to think.

Your dog or cat deserves your best thinking on the funding side, the same way they deserve your best thinking on every other dimension of their care. Get this right and the rest of their chronic disease management becomes considerably more sustainable across the years ahead.

Free downloads

Companion worksheets to put what you've read into practice. Free PDFs, print at home.

Sister tool · Sightline

Track whether treatment is working

Sightline, a separate ConciergeVet tool, runs a short weekly check-in built on validated pain and mobility instruments, turns it into a single Sightline Score you can watch trend over weeks rather than judge on one bad day, and produces a report you can bring to your vet.

A written log, or our printable trackers, does much the same job.

See how Sightline tracks treatmentSee where your pet stands today

Tracking is the other half of managing arthritis. Take the 2-minute Mobility Check to see your pet's stage, then watch it shift as treatment takes effect.

Take the Mobility CheckYou're not doing this alone

Compare treatment journeys and talk to owners managing arthritis. Free to join.

Join PetsLikeMine