Does pet insurance cover dental? Accident vs illness, decoded

Claire Greenway

BVM&S MRCVS

You've just had the news at the practice desk. The dental went well, a few teeth came out, your dog is groggy but comfortable, and the bill is a few hundred pounds. You hand over your insurance details, quietly relieved that this is exactly what you pay the premium for. Then, a fortnight later, the claim comes back rejected. "Dental," the letter says, as if that one word explains everything.

I've watched this happen to careful, well-meaning owners more times than I can count, and it is genuinely one of the most demoralising surprises in pet ownership. You did the responsible thing, you treated a painful mouth, and the safety net you'd paid into for years wasn't there. So before you're standing at that desk, let's decode how pet insurance actually treats dental work in the UK, why so much of it is excluded, and how to read your own policy tonight rather than after the bill lands.

Why "does it cover dental?" rarely has a yes-or-no answer

Here is the thing that trips everyone up. Whether a dental is covered doesn't depend only on your insurer. It depends just as much on why the tooth needs treating in the first place. Two dogs can have the same procedure, the same bill, and the same insurer, and one claim gets paid while the other doesn't.

The Association of British Insurers puts it plainly: cover for dental treatment varies right across the market, "from some insurers offering no cover, some offering accident only cover, to some offering full cover" (ABI, 2026). That single sentence is worth sitting with, because it means there is no such thing as "what pet insurance covers for teeth". There is only what your policy covers, and the only way to know is to read it. I'm not going to tell you which insurer to buy, and this isn't financial advice. What I can do is teach you to read the fine print like a vet reads a set of dental notes, so the categories stop being jargon.

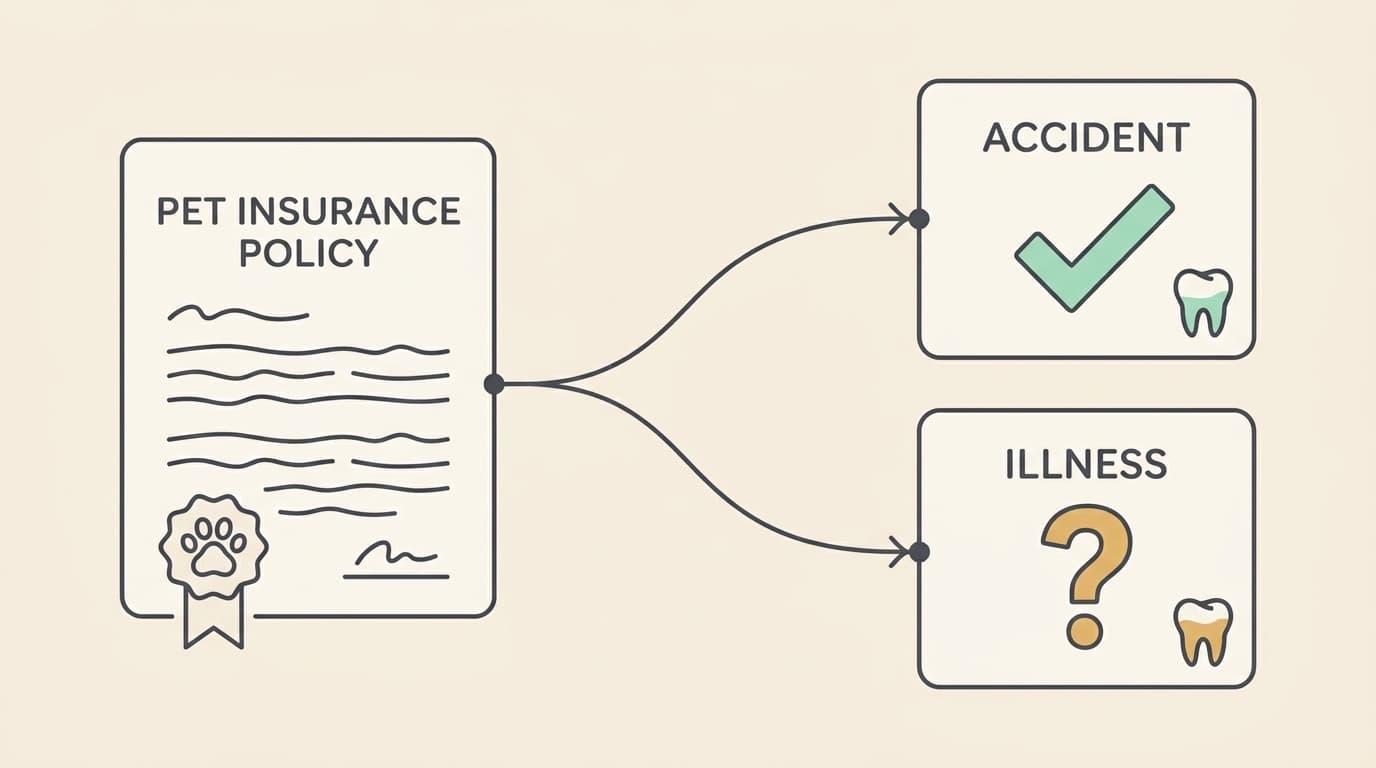

The split that decides everything: accident or illness

Most policies sort dental treatment into two buckets, and which bucket your pet's problem falls into usually decides whether you're paid.

Dental due to an accident means a sudden, external injury. Your dog runs into a fence and fractures a canine, or takes a knock to the jaw in the park. This is the kind of dental work that's most commonly covered, and even basic "accident only" policies will often include it (ABI, 2026; Vet Help Direct, 2026).

Dental due to illness means disease that developed over time from the inside: periodontal (gum) disease, a tooth-root abscess, tooth resorption, the everyday grinding-down of a mouth that needed a clean and some extractions. This is where the exclusions and conditions cluster, and it is also, by a wide margin, the reason most pets actually need a dental. Some policies cover dental illness in full, some cover it only if you meet a list of conditions we'll come to, and some don't cover it at all (ABI, 2026).

You can see the trap forming already. The dental work owners most often face is the illness kind, and that's precisely the kind an "accident only" or a cheaper tier may leave out entirely.

It's worth being honest about where the accident-or-illness line gets blurry, because insurers and owners don't always draw it in the same place. A slab fracture from an antler or a bone is the classic argument-starter. You'll call it an accident, because the tooth broke suddenly. An insurer may treat it as a foreseeable consequence of chewing something too hard, closer to wear than to trauma. There's no universal rule here, so if a chew has cracked a tooth, the wording of your specific policy matters enormously (Vet Help Direct, 2026). It's one more reason to keep hard chews out of the house in the first place, which we cover in [dangerous chews].

Where this hits cats hardest

Cats deserve their own paragraph here, not a footnote, because the accident-or-illness split lands very differently for them. The two big dental problems in cats are tooth resorption and feline chronic gingivostomatitis, and both are firmly illness. Cats also rarely present with the kind of dramatic accidental tooth trauma a boisterous dog does. What that means in practice is stark: an "accident only" policy, or a tier that excludes dental illness, offers a cat almost nothing for the dental disease it's genuinely likely to face. If you have a cat and dental cover matters to you, the illness half of the policy is the half that counts. You can read more about these conditions in [tooth resorption] and [feline chronic gingivostomatitis (FCGS), explained].

Routine cleaning: the bit that's almost never covered

Let's clear up the one part that's actually simple. A routine scale and polish, done to keep a reasonably healthy mouth in good order, is essentially never covered. It sits in the same excluded box as vaccinations, flea and worm treatment, nail clips and grooming, because insurers class it as preventive maintenance rather than treatment of a problem (ABI, 2026). ManyPets, for instance, states outright that its dental cover "doesn't include routine care, like a scale and polish", the one exception being where that cleaning is needed following an accident (ManyPets, 2026).

This catches people out because the line between "routine clean" and "treatment of disease" feels fuzzy from the owner's chair. From the insurer's side it's a real distinction: a preventive polish on a grade 1 mouth is routine, whereas a general anaesthetic to treat established periodontitis, take x-rays and remove diseased teeth is treatment. If you're bracing for the cost of either, [what a dental costs in the UK] walks through why the quotes vary so much.

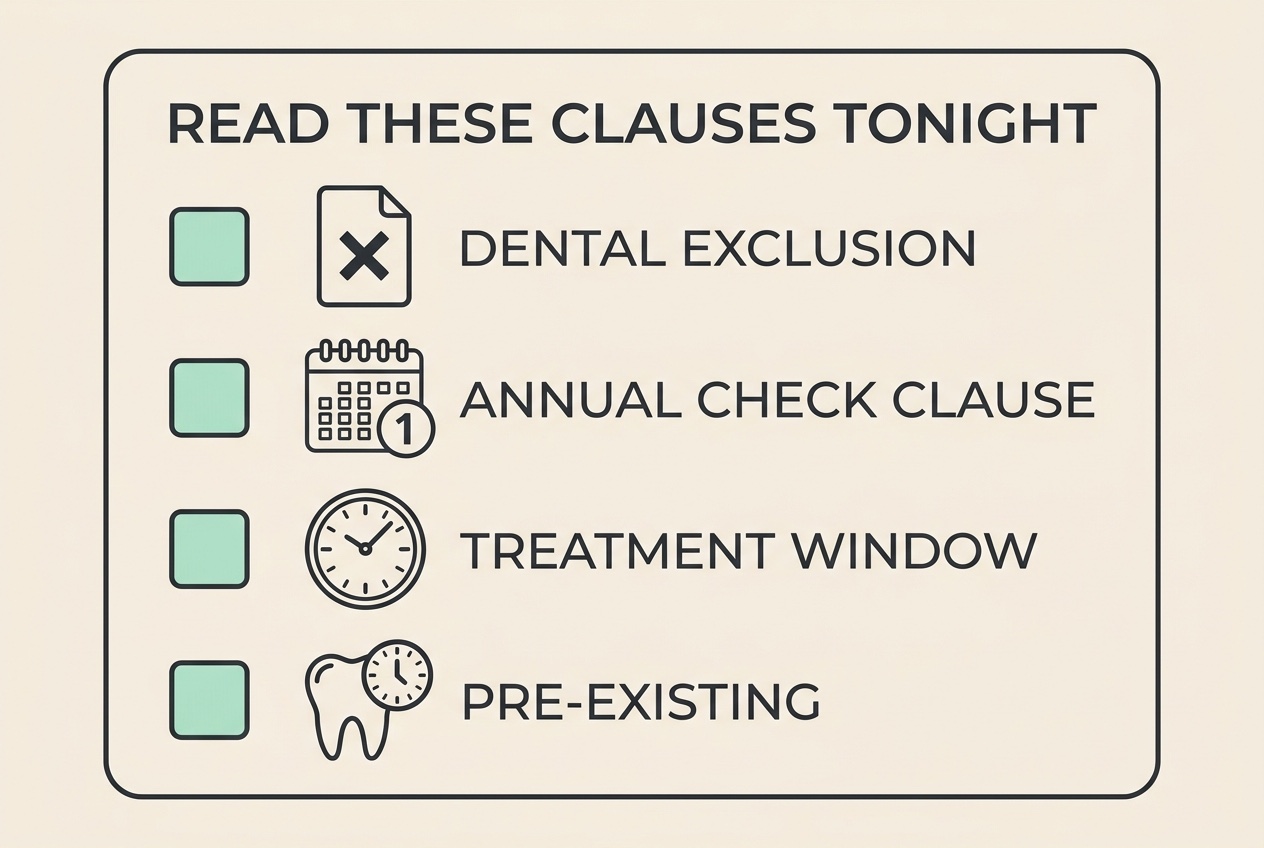

The clauses that get claims rejected

This is the part almost nobody reads until it's too late, and it's where that rejected claim at the top of this article usually comes from. Even when a policy does cover dental illness, it tends to cover it conditionally. Three conditions do most of the damage.

The annual dental check, and the treatment window. This is the big one, and it's genuinely reasonable once you understand it, but it catches thousands of owners every year. Several insurers will only pay a dental-illness claim if your pet has had a dental examination by a vet within the previous year, and you've had any treatment the vet recommended carried out within a set window. Petplan's condition is that you "arrange and pay for your pet to have an annual dental examination by a vet... and get any treatment they recommend to be carried out within 6 months" (Petplan, 2026). ManyPets says almost exactly the same, that it can't pay claims "where there has been no annual dental check-up or where dental treatment isn't completed within six months of an expert's recommendation" (ManyPets, 2026). Other insurers set the window at three months, or around seven.

Read that carefully, because it's the quiet killer. If your vet flagged at last year's check that your dog needed a dental, and life got busy and you booked it eight months later, the claim for that dental can be refused, even though the treatment was exactly what the vet advised. The clause isn't there to trap you; it exists because insurers want dental disease treated early, before it becomes an expensive mouthful of extractions. But it means an annual check and prompt action aren't just good for your pet, they're often the condition that keeps your cover alive.

Waiting periods. Almost every policy has a gap between the day you buy it and the day cover for illness begins, commonly around 14 days for illness (accidents are often covered sooner) (Vet Help Direct, 2026). Anything that arises in that window is treated as if it were there before you bought the policy.

Pre-existing exclusions. This is the one that quietly rules out more dental claims than any other, and it's baked into the nature of dental disease. Insurers won't cover a condition your pet "had or showed signs of having before the policy started" (ABI, 2026). Dental disease is extraordinarily common, most dogs and cats show some degree of periodontal disease by the age of three, so if your vet has ever noted tartar, gingivitis or a dental grade in the records before your policy began, or during the waiting period, gum disease can be treated as pre-existing and excluded from the off. It's not an insurer being awkward. It's the same rule that applies to a dodgy knee or a heart murmur, applied to a mouth that, statistically, was probably already showing early change.

How to read your own policy before you need it

The good news is you can settle all of this in one quiet evening, long before there's a bill in play. Here's how I'd go about it.

Start with the policy wording or terms and conditions document, not the glossy summary. Use the search function and look for the words "dental" and "teeth". You're trying to answer four questions in order:

- Is dental covered at all, and is it accident-only or accident-and-illness? This is usually stated near the top of the dental section or in the list of what's excluded.

- Is there an annual dental check condition, and is there a time limit for carrying out recommended treatment? Note the exact window, three months, six, or otherwise.

- What counts as pre-existing, and has my pet's mouth already been noted in the vet's records? If you're not sure, you can ask your practice for a copy of the history.

- What are the waiting periods, and any limits or excess specific to dental?

If any of that is unclear, ask the insurer directly and get the answer in writing, by email or through their message centre rather than over the phone, so you have a record. A fair question to put to them is simply: "Under this policy, in what circumstances would you decline a dental claim?" How readily they answer tells you a lot. And do all of this before you book a dental, not after, because once treatment is done the categories are fixed and there's nothing left to clarify.

One firm line from me, though, and I mean it as your vet, not your insurer: never let the state of your cover decide whether a painful, infected mouth gets treated. Insurance is there to soften the cost, not to grant permission. If your pet needs a dental and the claim turns out not to be covered, that's a frustrating bill, but a mouth left in pain and infection is a far worse outcome, and there are usually ways to spread or manage the cost with your practice. The untreated-mouth path is the one that genuinely harms the pet.

The two things that protect both your cover and your pet

There's a neat symmetry hiding in all of this, and it's the note I'll leave you on. The very habits that keep your dental cover valid are the same ones that reduce the chance you'll ever need to claim.

Keep up the annual dental check and act on what the vet recommends within the window your policy sets. That single habit satisfies the clause that rejects the most claims, and it means disease is caught while it's small and cheap rather than advanced and painful. Then do the daily home care that actually works, brushing above all, backed by products that have earned their evidence, which we lay out in [what actually works: chews, diets and water additives] and [brushing a dog's teeth]. A mouth that's brushed and checked is a mouth that's less likely to need the very treatment you're worried about paying for.

So tonight, before anything else: open your policy, find those four clauses, and diarise your pet's next dental check. That's the whole job. Do it now, while there's no bill on the table and no pressure in the room, and you'll never have that demoralising moment at the desk.

This article explains how UK pet insurance policies are typically structured. It is general guidance, not financial or insurance advice, and no rule here is universal. Policies vary widely between insurers and between tiers, and wording changes over time, so always check your own policy documents and confirm anything important with your insurer in writing.

References

- Association of British Insurers (ABI). What pet insurance does not cover. ABI Pet Insurance Guide. (accessed 2026)

- Petplan. Why does my pet have to have an annual dental check? Petplan Help Centre / FAQs. (accessed 2026)

- ManyPets. Does my pet insurance policy cover dental treatment? ManyPets Help. (accessed 2026)

- Vet Help Direct. Do any pet insurers cover dentistry in 2026? Vet Help Direct blog, 15 July 2026.

Keep track of how your pet is doing

The owners who cope best are the ones who notice changes early. A simple health log shows you what is working, and what is not, before the next vet visit.

Start tracking, freeYou're not doing this alone

Compare treatment journeys and talk to owners managing teeth & mouth. Free to join.

Join PetsLikeMine