What Does Cancer Treatment Cost, and How Do People Pay for It?

Claire Greenway

BVM&S MRCVS

"And roughly what does that cost?" is one of the hardest questions for an owner to ask, and one of the most sensible. A lot of people swallow it, as though loving a pet properly means money shouldn't come into it. It should, and it does. The cost of cancer treatment is a real constraint in a real life, and a good vet would much rather talk it through with you openly than watch you agonise quietly or, worse, put off coming in at all.

So this piece is that conversation, set out plainly. I'll give you realistic UK figures, explain how the money side actually works, and go through the ways people manage it. And I'll be straight about the thing that matters most: if treatment isn't affordable, you are not left with nothing. Comfort-focused care is real, loving, proper care, and choosing it for reasons that include cost does not make you a bad owner.

It's okay to think about money

Having a budget doesn't make you a worse owner, and asking what something costs before you agree to it isn't letting your pet down. It's the responsible thing to do, because a plan you can't sustain isn't really a plan. It's a problem waiting to surface halfway through a course of treatment.

Vets know this. The cost conversation is a normal part of working out what to do, and the best plans are built around what you can genuinely manage rather than the most expensive thing on the menu. When your vet talks you through the options, it's entirely fair to ask "and roughly what would each of those cost?" That's not awkward, and it's the question they're expecting.

The real UK numbers, as ranges

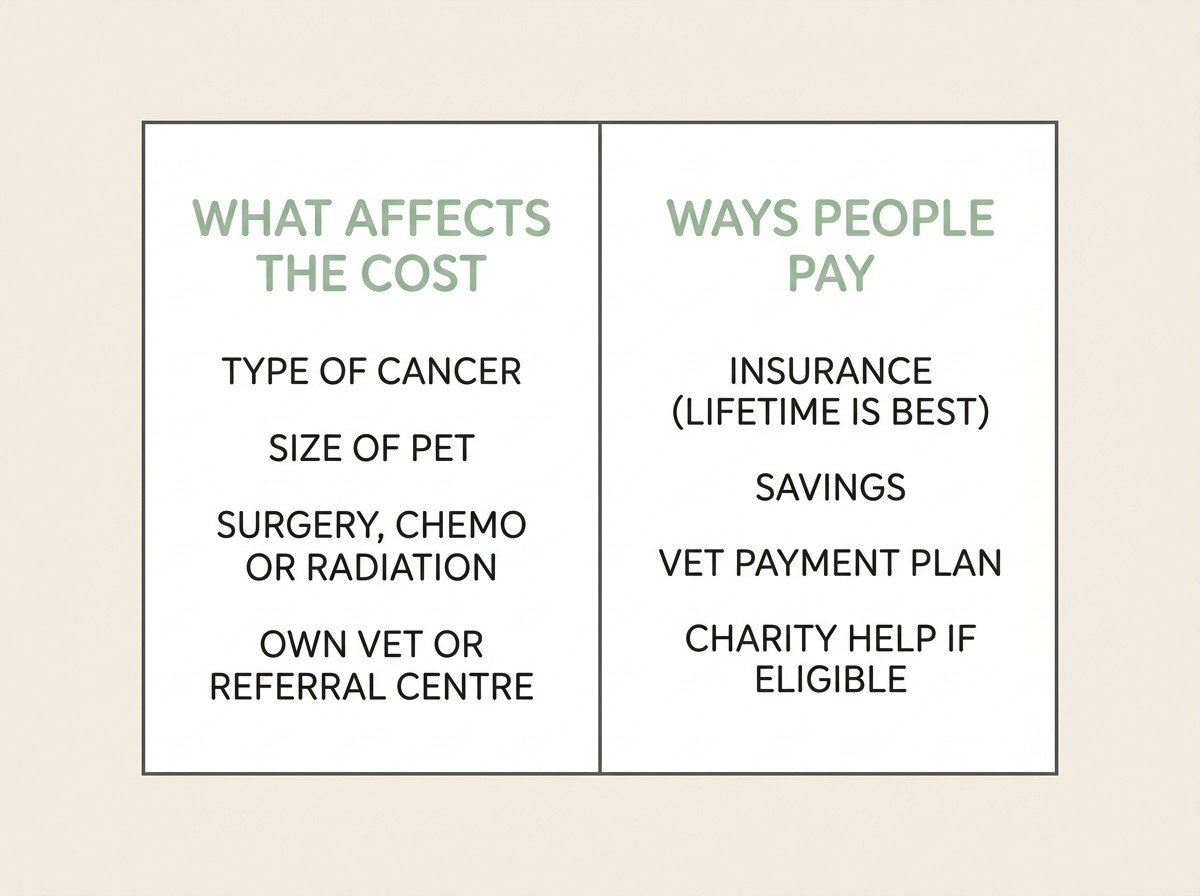

I can give you ballpark figures, but please read them as ranges rather than prices. What you'll actually pay depends on your pet's size, the type of cancer, where you live, and whether you're treated at your own practice or referred to a specialist centre. Referral oncology costs more, and most chemotherapy and radiation happens there. Treat everything below as what this tends to run to, and always ask for a written estimate for your own pet.

- The initial work-up (diagnosis and staging). Getting to a firm diagnosis and finding out how far things have spread, the consultations, blood tests, samples and scans, commonly runs from a few hundred pounds up to around £800 to £2,500 if advanced imaging is involved (PetCoverHQ, 2025; Paragon Veterinary Referrals, 2025).

- Surgery to remove a tumour. Hugely variable, but a cancer removal tends to fall somewhere around £1,500 to £4,000 depending on how complex it is and what's involved (PetCoverHQ, 2025; Paragon Veterinary Referrals, 2025).

- A course of chemotherapy. Intravenous chemotherapy commonly comes to around £2,500 to £5,000 over the full course (PetCoverHQ, 2025). Gentler oral (metronomic) protocols can be cheaper month to month, in the region of £200 to £400 a month, but run for longer (PetCoverHQ, 2025; Paragon Veterinary Referrals, 2025). Veterinary chemotherapy is dosed quite differently from human chemotherapy, and the [reality of pet chemo] surprises most people, which is worth reading before you weigh the cost.

- Radiation therapy. The big-ticket item, because it needs specialist equipment and repeated anaesthetics, often reaching up to around £9,000 for a full course (PetCoverHQ, 2025; Paragon Veterinary Referrals, 2025).

Put together, an involved course of specialist cancer treatment can realistically land in the £5,000 to £10,000 region (ManyPets, 2026). That's a frightening figure to read cold, so two bits of context. A great many pets never need the top end of it, and plenty are managed well at their own practice for far less. And that number is precisely why insurance, and the other routes below, matter so much.

How pet insurance actually works (and why the policy type decides everything)

Insurance is how most people who treat cancer afford it, but only if the policy is the right shape and was in place before the cancer appeared. UK pet insurance comes in a few types, and the differences aren't small print. They decide whether you're covered at all.

Lifetime cover is the type you want for something like cancer. It gives you a pot of money (an annual limit) that refills every year you renew, so a long-running condition can keep being claimed for year after year (CompareMyVet, 2025; GoCompare, 2025). As long as you keep renewing the same policy without a break, the insurer can't suddenly drop a condition just because you claimed for it last year. For a disease that can mean months or years of treatment and rechecks, that continuous cover is the whole point.

Annual (time-limited) cover is cheaper and works very differently. It typically covers a condition for only 12 months from when it first appears, or up to a set amount, and after that the condition is excluded at renewal as "pre-existing" (CompareMyVet, 2025). For a cancer that needs ongoing care, the cover can run out while your pet is still being treated.

Per-condition (maximum benefit) cover gives a fixed sum per condition with no time limit, but once you've used up that condition's pot, it's gone and won't refill.

Three more things catch people out, so they're worth knowing now.

- Pre-existing conditions are not covered, by anyone. Insurance only covers conditions that first show up after the policy starts. This is also why switching insurers after a diagnosis is usually a bad idea: the cancer becomes a pre-existing condition with the new insurer and won't be covered, even though your old policy would have continued it (Money Helper). If your pet is insured and unwell, think very hard before changing providers.

- The annual limit is a ceiling. Even on a good lifetime policy, claims are paid up to your annual limit, which is why a higher limit is worth having for a condition like this. Check what yours actually is.

- The excess (and sometimes a co-payment). You pay a fixed excess per condition per policy year, commonly around £85 to £120 (Pet Insurance Hub, 2025). Many policies also add a percentage co-payment, often 10% to 20%, that you pay on top once your pet reaches a certain age, frequently from around eight to ten years old (Pet Insurance Hub, 2025; CompareMyVet, 2025). On a £1,000 bill with a £100 excess and a 20% co-payment, you'd pay £280 of it and the insurer the rest. None of this is hidden, but it's worth reading your wording so the figure on the day isn't a surprise.

One more note. The average UK pet insurance claim for cancer in dogs has been reported at around £748 (ManyPets, 2026), which sounds reassuringly modest. But that average is dragged down by the many pets who have a single procedure or palliative care, and the pet who needs a full treatment course sits far above it. Plan around your policy's limits, not around an average.

If you're not insured, or the cover isn't enough

This is where a lot of owners feel cornered, so let's open up the options, because there are more of them than people think.

Savings, and a frank conversation about staging the spend. If you're paying out of pocket, ask your vet whether the work-up and treatment can be approached in steps, so you find out the realistic outlook before committing to the most expensive part. Sometimes a smaller, cheaper intervention buys good time without the full course.

A payment plan with your practice. Many practices will spread the cost or work with a pet-specific finance arrangement. It's always worth asking, ideally before treatment starts rather than after.

Charity help, if you're eligible. UK animal charities run veterinary services for owners on a low income, and these are a genuine lifeline, though they have real limits, eligibility rules, and usually a local catchment.

- PDSA provides free and low-cost veterinary care to eligible owners who receive certain means-tested benefits (such as Universal Credit without the housing element, Pension Credit, Income Support, Jobseeker's Allowance, income-based ESA, or certain disability benefits, plus some retired pensioners on Council Tax bands A to D) and who live within the catchment area of a PDSA Pet Hospital or Pet Clinic (PDSA). Free treatment is generally limited to one pet per eligible household, with reduced-cost care for others. Their role here tends to be subsidised treatment, pain relief and palliative care for eligible owners rather than full specialist oncology, but for keeping a pet comfortable it can matter enormously.

- Blue Cross runs low-cost veterinary services for owners on qualifying benefits or the State Pension who live within the catchment of one of its animal hospitals (in London and Grimsby), checked by postcode, with registration renewed yearly (Blue Cross).

- The RSPCA can sometimes help owners on means-tested benefits with veterinary costs through local branches, but funds and the kind of help available vary a great deal from branch to branch, so you'd need to contact your local one (RSPCA).

The plain caveat with all three is that they're means-tested, catchment-limited and stretched, so they can't help everyone and rarely fund a full course of high-end treatment. If you're eligible, though, they're well worth approaching early rather than as a last resort.

Vet-school and clinical-trial routes. University veterinary teaching hospitals sometimes run cancer trials, which can occasionally reduce the cost of cutting-edge treatment, though they come with their own uncertainties. There's more on weighing those in [clinical trials and newer options], and a [referral to a veterinary oncologist] is usually the way in.

When treatment isn't affordable, comfort care is real care

I want to come back to where this started, because it matters most. If, after looking at all of it, the numbers simply don't work, you haven't run out of options and you haven't failed your pet.

Comfort-focused care, keeping your pet genuinely well and happy with good pain relief and attention to the things they love, is real veterinary care and a valid, loving choice in its own right. It isn't a consolation prize. Owners choose it for all sorts of reasons, and cost being one of them is entirely legitimate. We cover the decision itself in [treating, comfort care and why there's no wrong answer], and how to do [comfort-focused care] well, because it deserves to be done properly rather than treated as "nothing".

So here's where to start, whichever way this goes. Ask your vet for a written estimate for each option, so you're working from real numbers rather than dread. Dig out your insurance policy and check the type, the annual limit, the excess and any co-payment, and don't switch insurers while your pet is unwell. And if money is tight, say so, plainly and early, because that one sentence is what lets your vet help you find a path your pet, and your life, can actually sustain.

References

- PDSA (People's Dispensary for Sick Animals). Eligibility FAQs. (eligibility checker: https://www.pdsa.org.uk/pet-help-and-advice/eligibility)

- Blue Cross. Low-cost vet treatment: Check eligibility.

- RSPCA. Veterinary financial assistance in your local area.

- CompareMyVet. Lifetime vs Annual Pet Insurance UK: What's the Difference? (2025).

- GoCompare. Compare Lifetime Pet Insurance.

- MoneyHelper. Pet insurance: do you need it?

- Pet Insurance Hub. Pet Insurance Excess Explained UK 2025: How It Works and What to Choose.

- ManyPets. How much is a vet visit in the UK? (updated 26 January 2026; average dog cancer insurance claim £748.17; advanced oncology £5,000–£10,000).

- PetCoverHQ (2025). Dog Cancer Treatment Costs in the UK: What Pet Owners Need to Know (UK £ ranges: staging incl. advanced imaging £800–£2,500; surgical removal £1,500–£4,000; IV chemotherapy £2,500–£5,000; oral metronomic £200–£400/month; radiation up to ~£9,000).

- Paragon Veterinary Referrals, Wakefield. General Cancer Q&A (UK referral-centre cost guidance corroborating the above: diagnosis/staging £800–£1,200, with CT £1,500–£2,200; mass excision £2,500–£3,500, more complex up to £4,500; injectable chemotherapy £300–£500 per treatment over ~3 months; oral metronomic £200–£400/month; radiation £3,000–£10,000 depending on protocol).

Free downloads

Companion worksheets to put what you've read into practice. Free PDFs, print at home.

Sister tool · Sightline

Track quality of life over time

Sightline, a separate ConciergeVet tool, runs a short adaptive weekly assessment with a quality-of-life focus mode built around exactly these frameworks, tracks a single composite score over time so you can see the trend rather than judge a single bad day, and produces a Sightline Report PDF you can bring to your vet.

A written log, or our printable quality-of-life sheet, does much the same job.

See how Sightline tracks quality of lifeFound a lump? Track it, and know when to act

A lump cannot be told apart by look or feel; only your vet sampling it can. The Lump & Bump Tracker records its size and how it changes, flags when it has crossed a line worth a vet visit, and builds a clean history to take in.

Open the Lump & Bump TrackerYou're not doing this alone

Compare treatment journeys and talk to owners managing cancer. Free to join.

Join PetsLikeMine